Study Notes

Overview

Break-even analysis is a cornerstone of business planning and financial management, and it is heavily tested across all GCSE Business specifications. Examiners expect candidates to not only perform calculations accurately but also to interpret break-even charts and evaluate the usefulness of this tool for business decision-making.

This study guide covers the definitions of fixed, variable, and total costs, the calculation of the break-even quantity and margin of safety, and the application of these concepts to real-world business scenarios such as pricing and marketing. Mastering this topic is essential for securing marks in both short calculation questions and extended evaluative essays.

Core Concepts

Business Costs

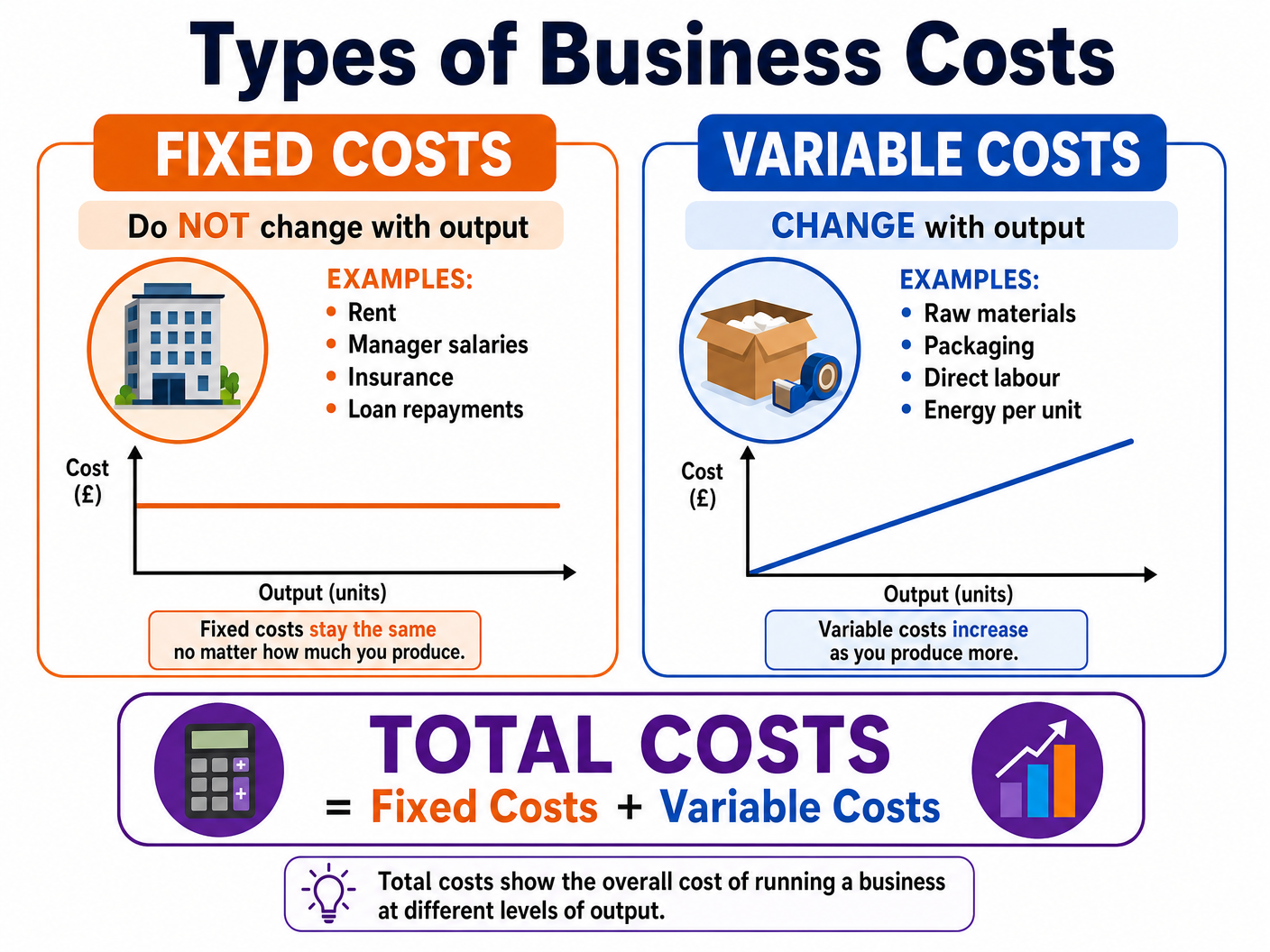

To calculate break-even, you must first understand the different types of costs a business faces:

- Fixed Costs: These are costs that do not change with the level of output in the short term. Whether a business produces zero units or 10,000 units, fixed costs remain the same. Examples include rent, insurance, and salaries.

- Variable Costs: These are costs that change directly with the level of output. As production increases, variable costs increase. Examples include raw materials, packaging, and piece-rate labour.

- Total Costs: The sum of fixed costs and variable costs (Total Costs = Fixed Costs + Variable Costs).

Revenue and Profit

- Total Revenue: The total amount of money brought in by sales. It is calculated by multiplying the selling price per unit by the number of units sold (Total Revenue = Price × Quantity).

- Profit: The financial gain made when total revenue exceeds total costs.

- Loss: The financial loss made when total costs exceed total revenue.

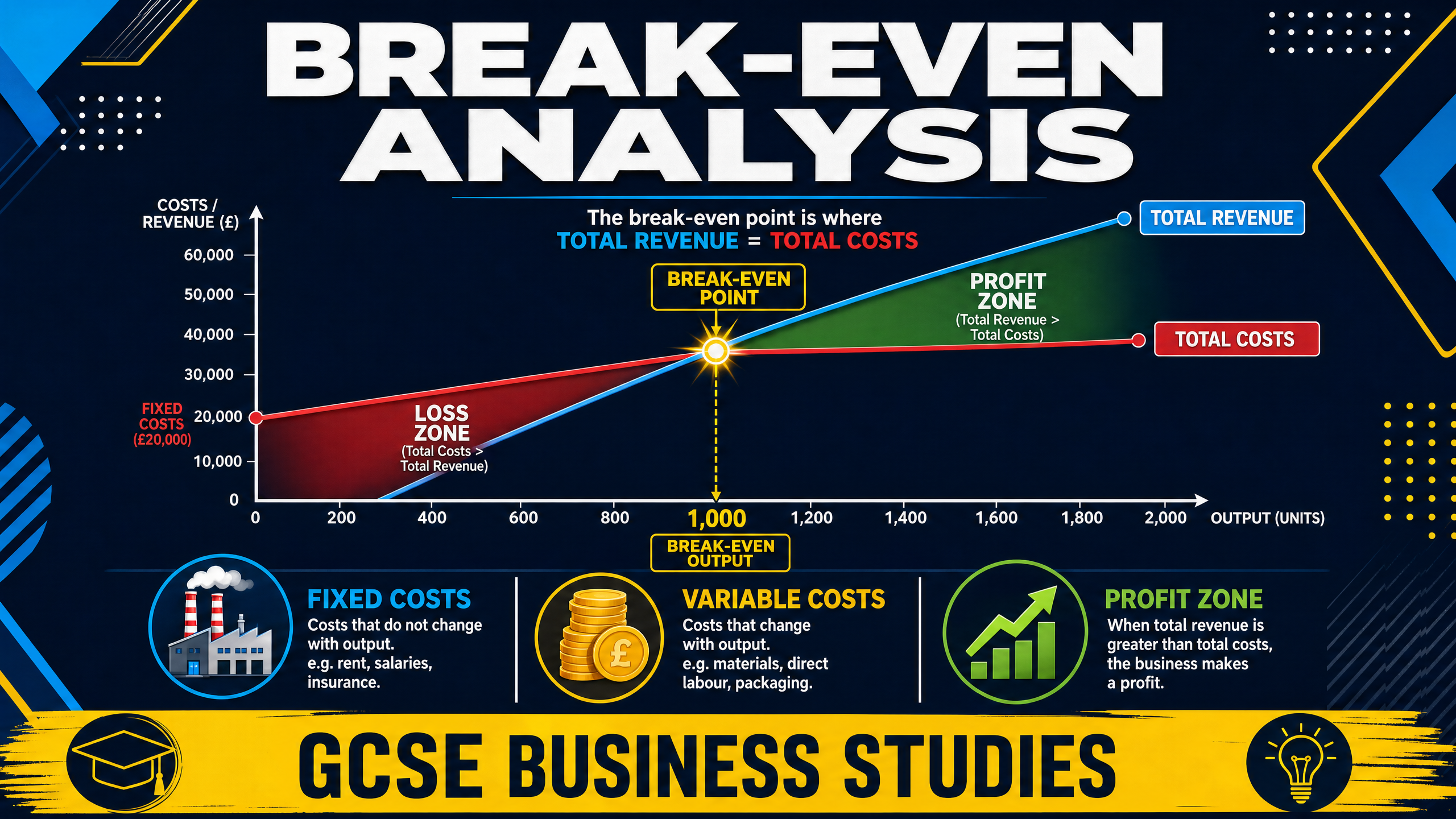

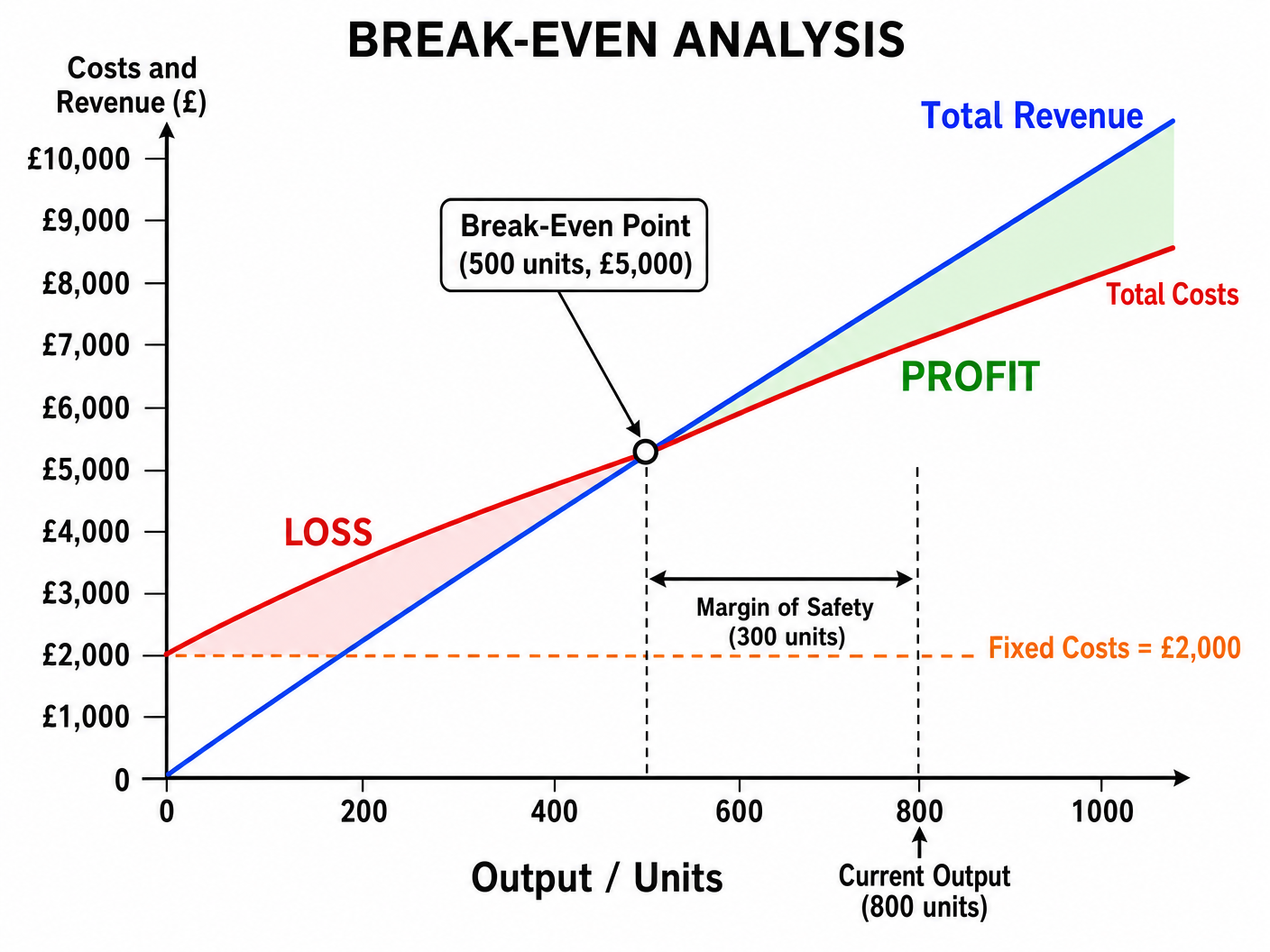

The Break-Even Point

Break-even is the point at which a business is making neither a profit nor a loss. At this exact level of output, Total Revenue = Total Costs.

Contribution

Contribution is a crucial concept for calculating break-even. It is the amount of money left over from the sale of each unit after variable costs have been paid. This 'contribution' goes towards paying off the fixed costs.

Contribution per unit = Selling Price - Variable Cost per unit

Calculating Break-Even Quantity

The formula to calculate the number of units a business needs to sell to break even is:

Break-Even Quantity = Fixed Costs / Contribution per unit

Margin of Safety

The margin of safety is the difference between the current (or expected) level of output and the break-even level of output. It shows how much sales can fall before the business starts making a loss.

Margin of Safety = Current Output - Break-Even Output

Break-Even Charts

Examiners often require candidates to draw, complete, or interpret break-even charts.

Key features of a break-even chart:

- X-axis: Output (units)

- Y-axis: Costs and Revenue (£)

- Fixed Costs Line: A horizontal line starting from the fixed cost value on the Y-axis.

- Total Costs Line: Starts from the fixed costs intercept on the Y-axis and slopes upwards.

- Total Revenue Line: Starts from the origin (0,0) and slopes upwards, usually steeper than the total costs line.

- Break-Even Point: The intersection of the Total Costs and Total Revenue lines.

Podcast Episode

Listen to this 10-minute podcast for a comprehensive review of Break-Even Analysis, including a step-by-step calculation walkthrough and a quick-fire recall quiz.

Worked Examples

3 detailed examples with solutions and examiner commentary

Practice Questions

Test your understanding — click to reveal model answers

A bakery has fixed costs of £5,000 per month. It sells cakes for £3 each. The variable cost per cake is £1. Calculate the break-even quantity. (3 marks)

Hint: Remember to calculate contribution per unit first.

Using the bakery from the previous question, if they currently sell 3,000 cakes a month, calculate their margin of safety. (2 marks)

Hint: Margin of Safety = Current Output - Break-Even Output

Explain one limitation of using break-even analysis for a business. (3 marks)

Hint: Think about the assumptions made when drawing a break-even chart.

A clothing manufacturer's rent increases by £1,000 a month. Explain the impact this will have on their break-even point. (3 marks)

Hint: Rent is what type of cost? How does an increase in this cost affect the formula?

State the formula for calculating total costs. (1 mark)

Hint: It's the sum of the two main types of costs.