Study Notes

Overview

This study guide covers one of the most fundamental concepts in GCSE Business: Stakeholders. A stakeholder is any individual, group, or organisation that has an interest in the activities and decision-making of a business. Examiners consistently test your ability to not only identify these groups but also to analyse their objectives and evaluate the conflicts that arise between them.

Understanding stakeholders is crucial because businesses do not operate in a vacuum. Every decision a business makes—from launching a new product to relocating a factory—has a ripple effect. In your exams, you will be expected to demonstrate how business activity affects stakeholders, and conversely, how stakeholders can influence business decisions.

Listen to the comprehensive podcast below for an examiner's perspective on this topic:

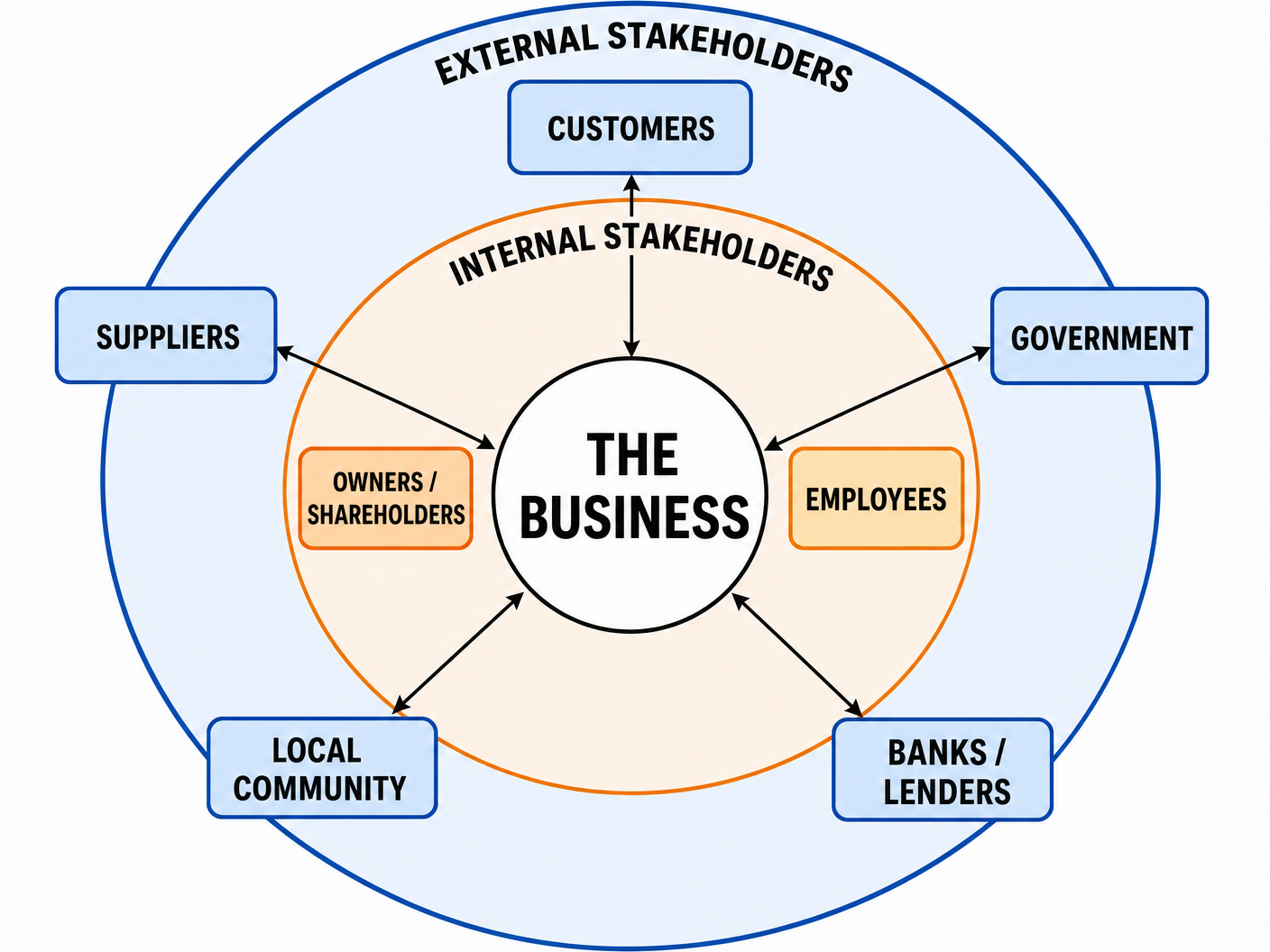

Internal vs External Stakeholders

Examiners frequently ask candidates to distinguish between internal and external stakeholders. Confusing the two is a common pitfall that will cost you marks.

Internal Stakeholders

Internal stakeholders are individuals or groups who are directly involved in the day-to-day operations or ownership of the business. They are 'inside' the organisation.

- Owners / Shareholders: In a sole trader or partnership, these are the owners. In a limited company, they are the shareholders. They invest capital into the business.

- Employees: The workforce who carry out the daily operations of the business in exchange for wages or a salary.

External Stakeholders

External stakeholders are individuals or groups who are outside the business but are still affected by its activities or can affect its operations.

- Customers: The people or other businesses that purchase the goods or services.

- Suppliers: The businesses that provide raw materials, components, or services required for production.

- Government: Local and national authorities that set the legal and tax framework.

- Local Community: The people who live and work in the area surrounding the business premises.

- Banks and Lenders: Financial institutions that provide loans and overdrafts.

Stakeholder Objectives

To achieve high marks, you must be able to explain the specific objectives of each stakeholder group. Generic answers will not suffice.

Owners / Shareholders

Objective: Profit maximisation, return on investment (dividends), business growth, and survival.

Impact of Business Activity: Successful decisions lead to higher profits and increased share value. Poor decisions lead to financial loss.

Influence on Business: Shareholders can vote at the Annual General Meeting (AGM) to appoint or remove directors. They also provide the necessary capital for expansion.

Employees

Objective: Job security, fair pay (wages/salary), good working conditions, and opportunities for promotion.

Impact of Business Activity: Expansion can create promotion opportunities, while automation or cost-cutting can lead to redundancies.

Influence on Business: Employees can influence productivity levels. Through trade unions, they can negotiate pay and, in extreme cases, take industrial action (strikes) which halts production.

Customers

Objective: High-quality products, value for money, excellent customer service, and increasingly, ethical business practices.

Impact of Business Activity: Product innovation provides better choices, while price increases or quality reductions negatively affect them.

Influence on Business: Customers vote with their feet. If they are dissatisfied, they will buy from competitors, directly reducing the business's revenue and market share.

Suppliers

Objective: Regular orders, prompt payment at fair prices, and long-term contracts for stability.

Impact of Business Activity: A business expanding its operations will increase order volumes, benefiting the supplier. A business struggling financially may delay payments.

Influence on Business: Suppliers can alter delivery times, change credit terms, or refuse to supply goods if they are not paid, which can bring a business's operations to a standstill.

Government

Objective: Legal compliance, job creation, and the payment of taxes (e.g., Corporation Tax, VAT).

Impact of Business Activity: Profitable businesses contribute more tax revenue and reduce local unemployment rates.

Influence on Business: The government passes legislation (e.g., National Minimum Wage, health and safety laws) that businesses must follow, and sets taxation rates that directly affect profit margins.

Local Community

Objective: Local employment opportunities, minimal environmental impact (noise, traffic, pollution), and socially responsible behaviour.

Impact of Business Activity: A new factory provides jobs but may increase congestion and pollution in the area.

Influence on Business: The community can object to planning permission applications, stage protests, or generate negative local PR, which can delay or halt business expansion plans.

Stakeholder Conflict

One of the most important analytical skills in GCSE Business is evaluating stakeholder conflict. This occurs when the objectives of one stakeholder group contradict the objectives of another.

Common Conflicts

- Shareholders vs. Employees: Shareholders want to maximise profits, which often involves keeping costs (including wages) low. Employees want higher wages. Paying higher wages directly reduces the profit available for dividends.

- Business/Shareholders vs. Local Community: A business may want to expand its factory to operate 24/7 to increase output and profit. The local community will likely oppose this due to increased noise, traffic, and potential pollution during the night.

- Customers vs. Shareholders: Customers want high-quality products at low prices. Shareholders want high profit margins. Keeping prices low to satisfy customers can reduce the profit margins that shareholders desire.

Examiner Tip: When analysing conflict, always explain why the conflict exists by clearly stating the opposing objectives, and then evaluate how the business might resolve it (e.g., offering profit-sharing schemes to align employee and shareholder interests).

Worked Examples

3 detailed examples with solutions and examiner commentary

Practice Questions

Test your understanding — click to reveal model answers

State two external stakeholders of a supermarket. (2 marks)

Hint: Think about groups outside the supermarket who interact with it.

Explain how a decision to switch to cheaper, lower-quality suppliers might affect customers. (3 marks)

Hint: What is the primary objective of a customer, and how does lower quality affect this?

Analyse the impact on two stakeholder groups if a business decides to close one of its high street stores to focus on online sales. (6 marks)

Hint: Choose one internal and one external group. How does store closure affect their specific objectives?

Evaluate whether the government is the stakeholder with the most influence over a business. (9 marks)

Hint: Argue why the government is powerful (laws, taxes), but counter-argue with another powerful group (like customers or owners).

A local coffee shop is considering extending its opening hours until 10 PM. Explain one stakeholder conflict this might cause. (3 marks)

Hint: Who benefits from longer hours, and who might be annoyed by it?