Economic Resources (Factors of Production) — OCR GCSE Study Guide

Exam Board: OCR | Level: GCSE

This study guide provides a comprehensive, exam-focused breakdown of Economic Resources (Factors of Production) for OCR GCSE Economics. It clarifies the four essential factors, their rewards, and how they are combined to address scarcity, ensuring candidates can secure maximum marks on this fundamental topic.

## Overview

This topic, Economic Resources (also known as the Factors of Production), is a cornerstone of the OCR GCSE Economics specification (J205). It explores the fundamental inputs required to produce all goods and services in an economy. Examiners expect candidates to demonstrate a precise understanding of the four factors: **Land, Labour, Capital, and Enterprise**. A mastery of this topic is crucial as it forms the basis for analysing business behaviour, market dynamics, and government policy. Candidates must not only define each factor but also identify its corresponding reward, analyse how entrepreneurs combine these resources to solve the basic economic problem of scarcity, and apply this knowledge to real-world case studies. Credit is consistently awarded for distinguishing between related concepts, such as capital goods and consumer goods, and for analysing the impact of factor mobility on productive efficiency. This guide will equip you with the specific knowledge and analytical skills required to excel.

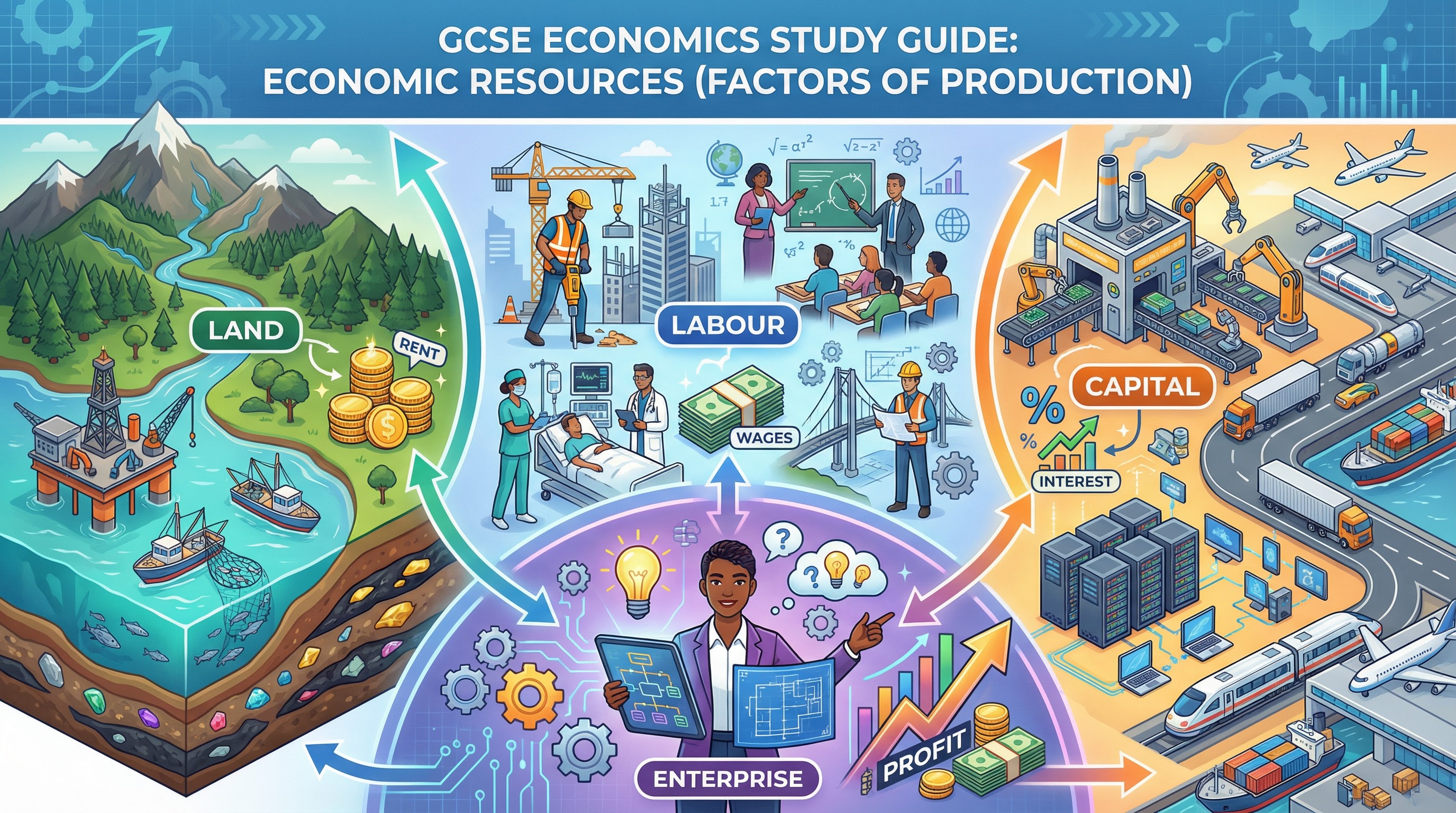

## The Four Factors of Production

### 1. Land

**Definition**: In economics, **Land** refers to all **natural resources** used in production. This is a much broader definition than the everyday use of the word.

**What it includes**: It encompasses not just physical territory or agricultural fields, but also raw materials and resources found on and under the earth. This includes:

- **Minerals**: Oil, natural gas, coal, diamonds.

- **Forests**: Timber, rubber.

- **Water**: Rivers, seas, and the fish within them.

- **Agricultural Land**: Soil used for growing crops.

- **Other Natural Elements**: Air, sunlight, and climate.

**Reward**: The reward for owning and providing the factor of Land is **Rent**. This is the income received by the owner of the natural resource.

**Examiner Tip**: A common mistake is to limit the definition of Land to just fields. Marks are awarded for explicitly stating that it includes all natural resources. For example, in a case study about the fishing industry, the fish are the 'Land' resource, while the fishing boat is 'Capital'.

### 2. Labour

**Definition**: **Labour** is the **human effort, both mental and physical**, that goes into the production of goods and services.

**What it includes**: It covers the work done by all individuals in the economy, from a construction worker building a house (physical effort) to a software developer writing code (mental effort). The quality of labour is a critical determinant of a country's productivity and can be improved through education, training, and healthcare.

**Reward**: The reward for providing Labour is **Wages** or a **Salary**.

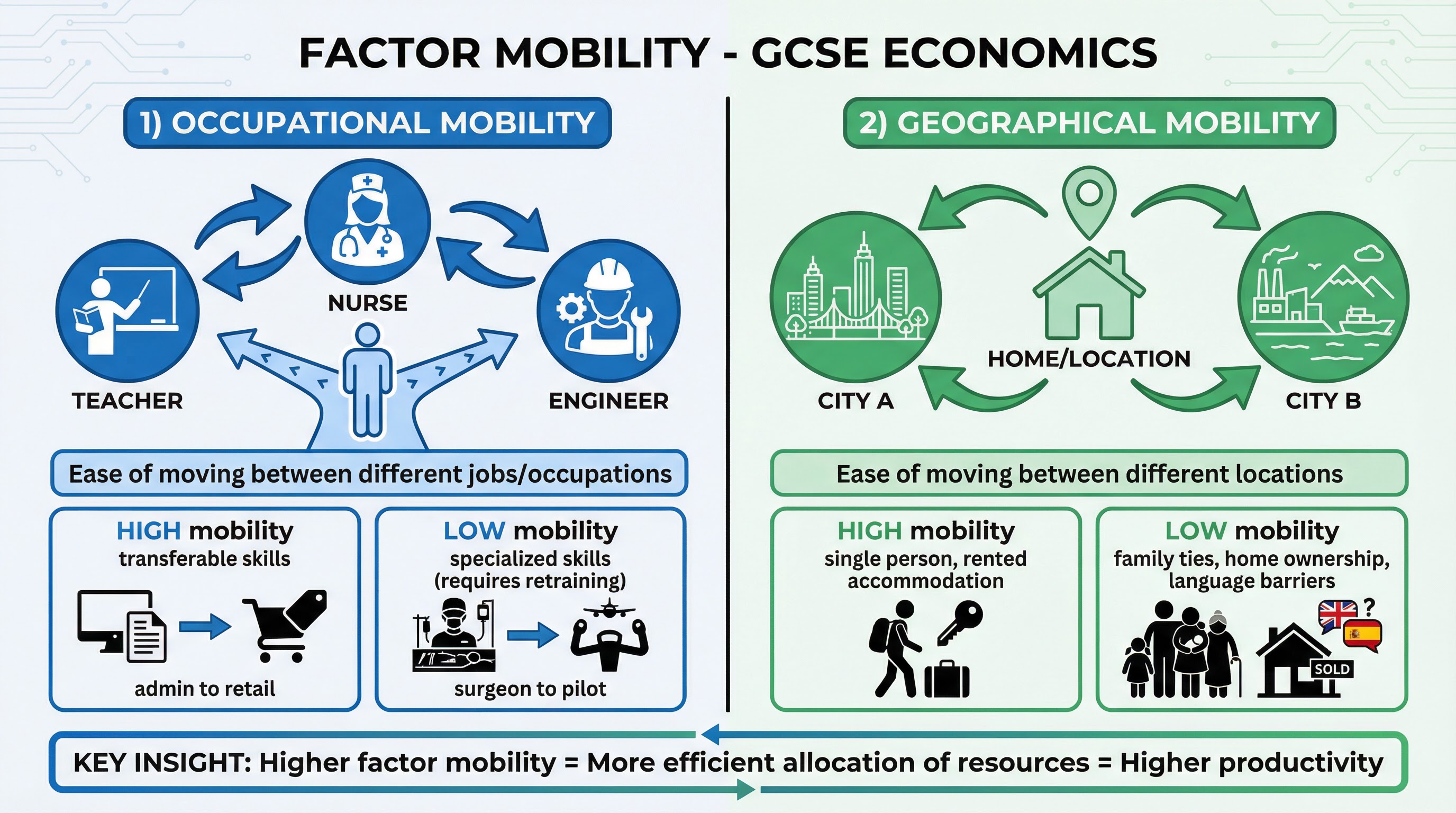

**Specific Knowledge**: Examiners credit candidates who can analyse the mobility of labour:

- **Occupational Mobility**: The ease with which a worker can move from one type of job to another. This is high for jobs with transferable skills (e.g., administrative roles) and low for highly specialized professions (e.g., a brain surgeon cannot easily become a pilot).

- **Geographical Mobility**: The ease with which a worker can move from one location to another for work. This can be affected by factors like family ties, housing costs, and language barriers.

### 3. Capital

**Definition**: **Capital** consists of **man-made aids to production**. These are goods that are not consumed for their own sake but are used to produce other goods and services.

**What it includes**: This is the area where candidates most frequently make errors. Capital is NOT money. It refers to physical assets such as:

- **Machinery and Equipment**: Factory assembly lines, tractors, computers.

- **Tools**: Hammers, drills, software.

- **Infrastructure**: Roads, railways, ports, internet cables.

- **Buildings**: Factories, offices, schools.

**Reward**: The reward for providing Capital is **Interest**. This is the payment made to those who lend money to firms to purchase capital goods.

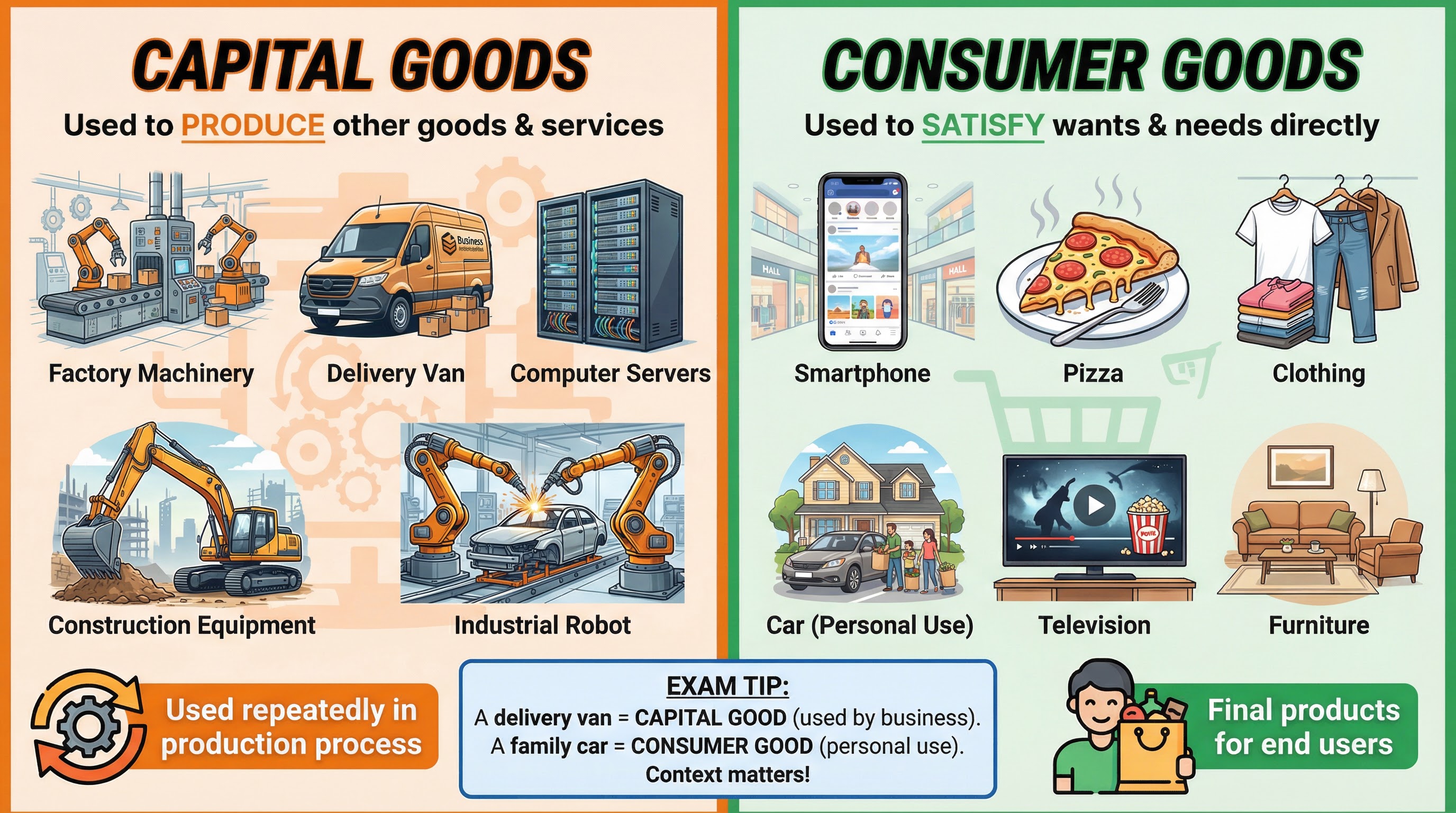

**Distinction**: It is vital to distinguish between **Capital Goods** and **Consumer Goods**.

- **Capital Goods**: Used to produce other goods (e.g., a delivery van, an oven in a bakery).

- **Consumer Goods**: Used to satisfy wants and needs directly (e.g., a personal car, a pizza).

### 4. Enterprise

**Definition**: **Enterprise** is the factor that organises the other three factors of production and, crucially, **takes the risks** associated with the business venture.

**What it includes**: The entrepreneur is the individual or group who:

- **Organises Production**: Brings together Land, Labour, and Capital in a productive process.

- **Makes Business Decisions**: Decides what to produce, how to produce it, and for whom.

- **Bears Risk**: Takes the financial risk of the business failing. If the business is unsuccessful, the entrepreneur may lose their personal investment.

- **Innovates**: Develops new products, services, or production methods.

**Reward**: The reward for Enterprise is **Profit**. This is the residual income left over after all other costs (rent, wages, interest) have been paid. It is an uncertain reward for successful risk-taking.

**Examiner Tip**: High-level answers will always emphasise the dual function of the entrepreneur: organising production AND bearing risk. Simply stating they 'manage' the business is not enough for top marks.