Finance Revision Notes

Introduction

Comprehensive revision notes for AQA GCSE.

Summary & Overview

Master the crucial calculations and concepts of GCSE Business Finance. This guide covers everything from cash flow forecasting to break-even analysis, ensuring you have the tools to evaluate financial decisions and secure top marks.

Study Material

## Overview

Welcome to Topic 3.6: Finance. This section of the GCSE Business specification is heavily weighted towards quantitative skills (AO2) and evaluation (AO3). Examiners expect candidates to not only perform calculations accurately but also to interpret the results within a specific business context. You will explore how businesses raise capital, manage their cash flow, calculate profit and loss, and assess their overall financial health using key statements.

## Key Financial Concepts

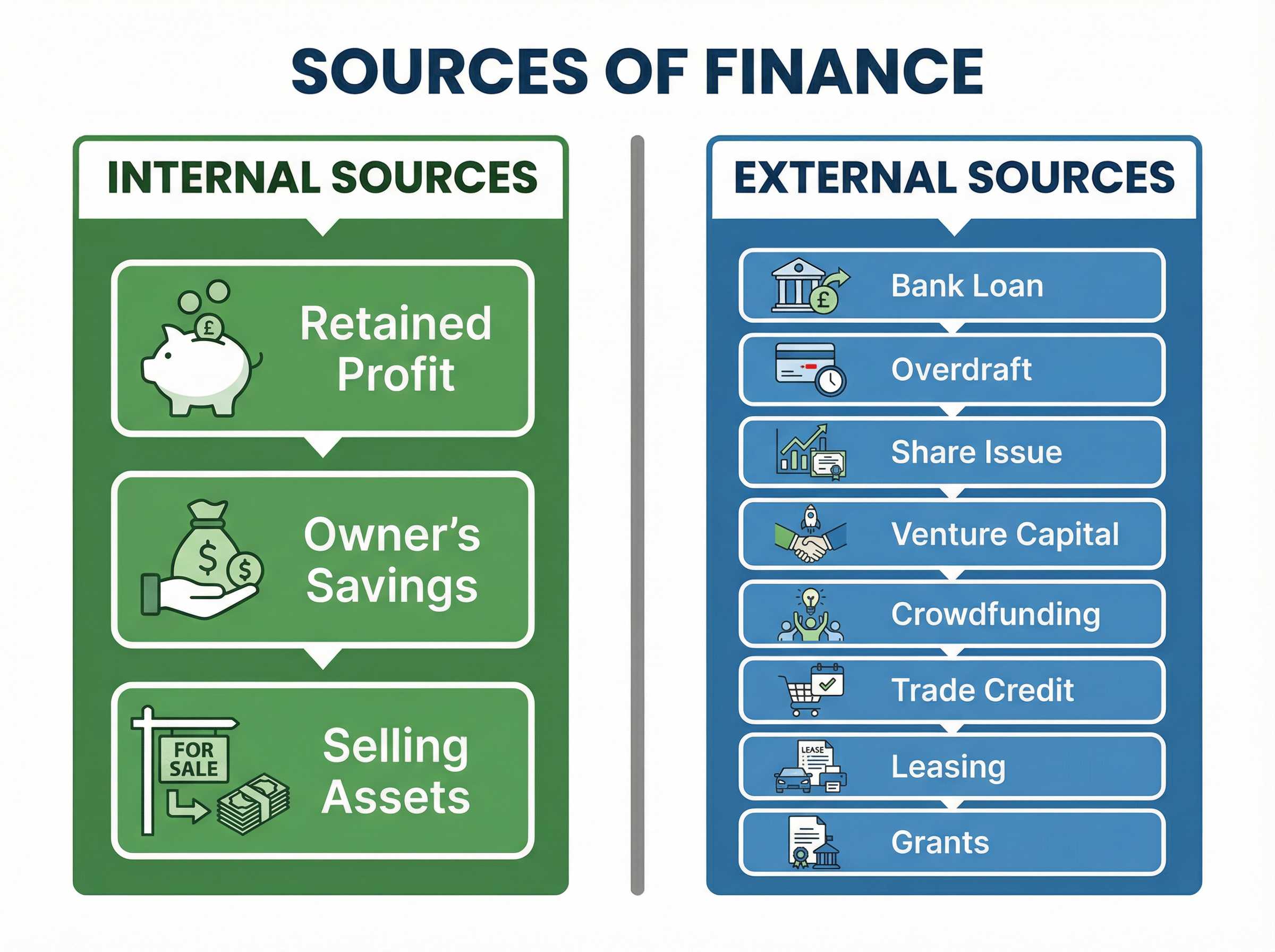

### Sources of Finance

Every business needs capital to start, operate, and grow. Examiners frequently ask candidates to evaluate the most appropriate source of finance for a given scenario.

**Internal Sources**:

- **Retained Profit**: Profit kept in the business after tax and dividends. It's cheap (no interest) but may not be sufficient for large investments.

- **Selling Assets**: Disposing of unwanted machinery or buildings to raise cash.

- **Owner's Savings**: Personal funds invested by the entrepreneur.

**External Sources**:

- **Bank Loan**: A fixed amount borrowed and repaid with interest over time. Suitable for long-term assets.

- **Overdraft**: A short-term facility allowing a business to withdraw more than its bank balance. High interest rates apply.

- **Share Issue**: Selling shares to raise capital (limited companies only). Does not need to be repaid, but dilutes ownership.

- **Venture Capital**: Investment from specialists in exchange for equity.

- **Crowdfunding**: Raising small amounts from a large number of people online.

- **Trade Credit**: Buying goods and paying for them later (e.g., 30 days).

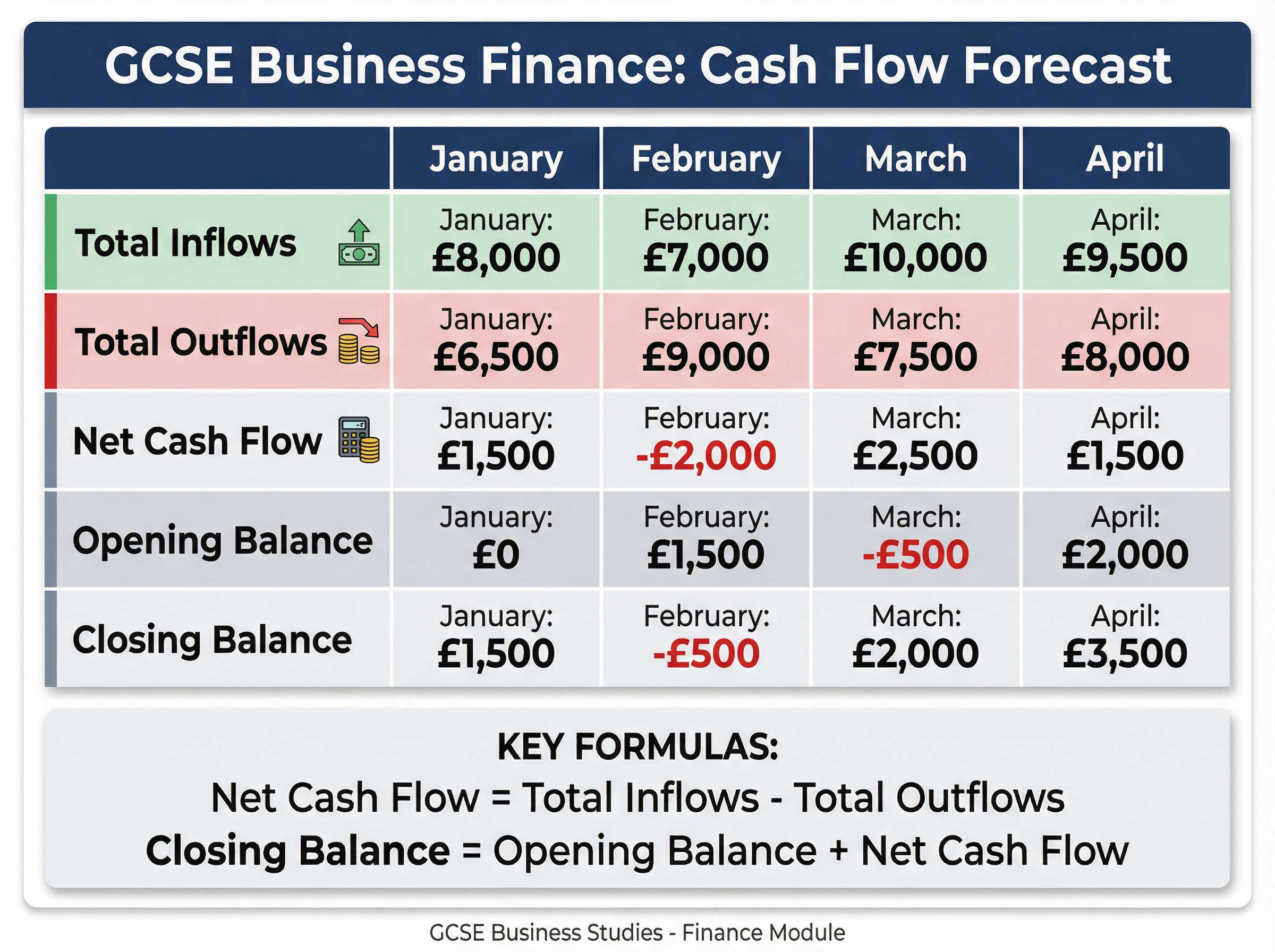

### Cash Flow Forecasting

A cash flow forecast predicts the inflows and outflows of cash over a future period. It is crucial for identifying potential liquidity problems before they occur.

**Key Formulae**:

- **Net Cash Flow** = Total Inflows - Total Outflows

- **Closing Balance** = Opening Balance + Net Cash Flow

**Examiner Tip**: A common mistake is confusing cash flow with profit. A business can be profitable but still fail due to poor cash flow (e.g., if customers delay payment).

### Costs, Revenue, and Profit

Understanding the relationship between costs and revenue is fundamental to calculating profit.

- **Revenue** = Selling Price × Quantity Sold

- **Total Costs** = Fixed Costs + Variable Costs

- **Profit** = Total Revenue - Total Costs

**Profit Margins** measure how efficiently a business converts sales into profit:

- **Gross Profit Margin** = (Gross Profit ÷ Revenue) × 100

- **Net Profit Margin** = (Net Profit ÷ Revenue) × 100

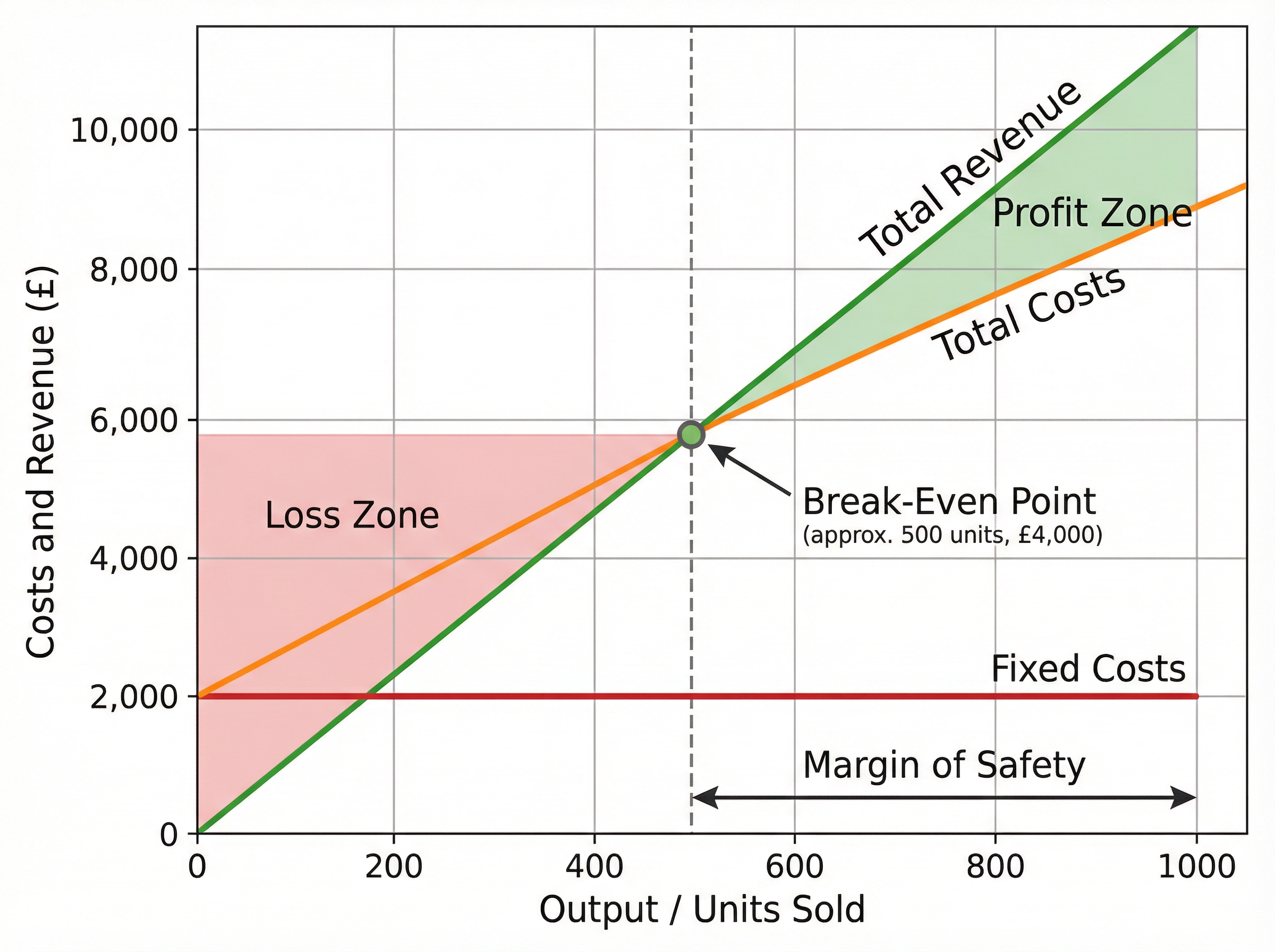

### Break-Even Analysis

The break-even point is the level of output where total revenue equals total costs. At this point, the business makes neither a profit nor a loss.

- **Contribution per Unit** = Selling Price - Variable Cost per Unit

- **Break-Even Output** = Fixed Costs ÷ Contribution per Unit

- **Margin of Safety** = Actual Output - Break-Even Output

### Average Rate of Return (ARR)

ARR compares the average annual profit of an investment with the initial cost, expressed as a percentage. It helps businesses decide whether an investment is worthwhile.

- **ARR** = (Average Annual Profit ÷ Cost of Investment) × 100

### Financial Statements

- **Income Statement (Profit & Loss Account)**: Shows revenue, costs, and profit over a period of time (usually a year).

- **Statement of Financial Position (Balance Sheet)**: A snapshot of what the business owns (assets) and owes (liabilities) on a specific date.

## Podcast Episode

Listen to the complete audio guide for Topic 3.6 Finance, featuring detailed explanations, exam tips, and a quick-fire recall quiz.