The purpose and nature of businesses Revision Notes

Subject: Business | Level: GCSE | Exam Board: AQA

This study guide introduces the fundamental purpose of business activity, the role of enterprise, and the dynamic nature of the business environment. It covers the core reasons for starting a business, the basic factors of production, the distinction between goods and services, and the crucial concept of opportunity cost. Mastering this topic is essential as it underpins everything else you will study in GCSE Business.

Revision Notes & Key Concepts

## Overview

This topic forms the foundation of your GCSE Business studies. It explores the fundamental questions of why businesses exist, what resources they need to operate, and how they fit into the wider economy. Examiners expect candidates to not only define key terms like 'opportunity cost' and 'factors of production', but also to apply them to real-world business scenarios. A strong grasp of the dynamic nature of business—how external changes force businesses to adapt—is crucial for accessing the higher mark bands in longer, analytical questions.

## The Purpose of Business

At its core, a business is an organisation that provides goods or services to satisfy customer needs and wants.

* **Needs**: Essential items required for survival (e.g., food, water, basic clothing, shelter).

* **Wants**: Desires that are not essential for survival but improve the quality of life (e.g., designer clothes, smartphones, holidays).

Businesses exist to close the gap between limited resources and unlimited human wants. People start businesses for various reasons, including to make a profit, to be their own boss, to fulfil a gap in the market, or to pursue a personal passion.

## The Four Factors of Production

To produce goods and services, businesses require resources, known as the factors of production. Examiners frequently test candidates' ability to identify and classify these resources.

* **Land**: Natural resources provided by the earth (e.g., oil, water, minerals, physical space).

* **Labour**: The human effort, skills, and knowledge contributed by workers.

* **Capital**: Man-made resources used to produce other goods and services (e.g., machinery, tools, buildings, vehicles). *Note: In this context, capital refers to physical assets, not just money.*

* **Enterprise**: The drive and innovation required to combine the other three factors, take risks, and start a business.

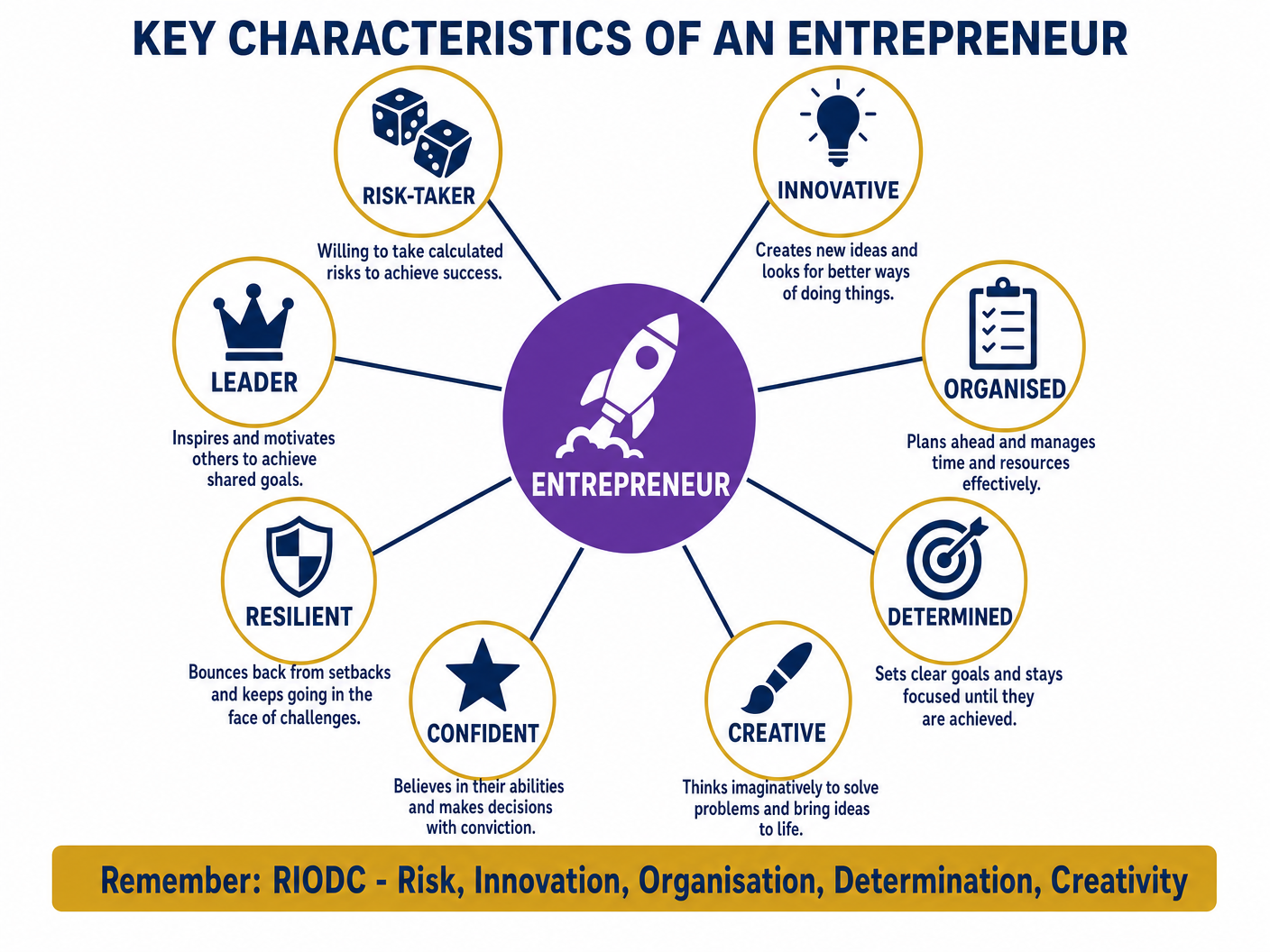

## The Role of the Entrepreneur

An entrepreneur is an individual who organises the factors of production, takes on financial risk, and aims to make a profit. They are the driving force behind new business ventures.

Key characteristics of successful entrepreneurs include:

* **Risk-taking**: Willingness to invest time and money with no guarantee of success.

* **Innovation**: Creating new ideas or finding better ways to do things.

* **Organisation**: Effectively coordinating resources.

* **Determination**: Persisting through challenges and setbacks.

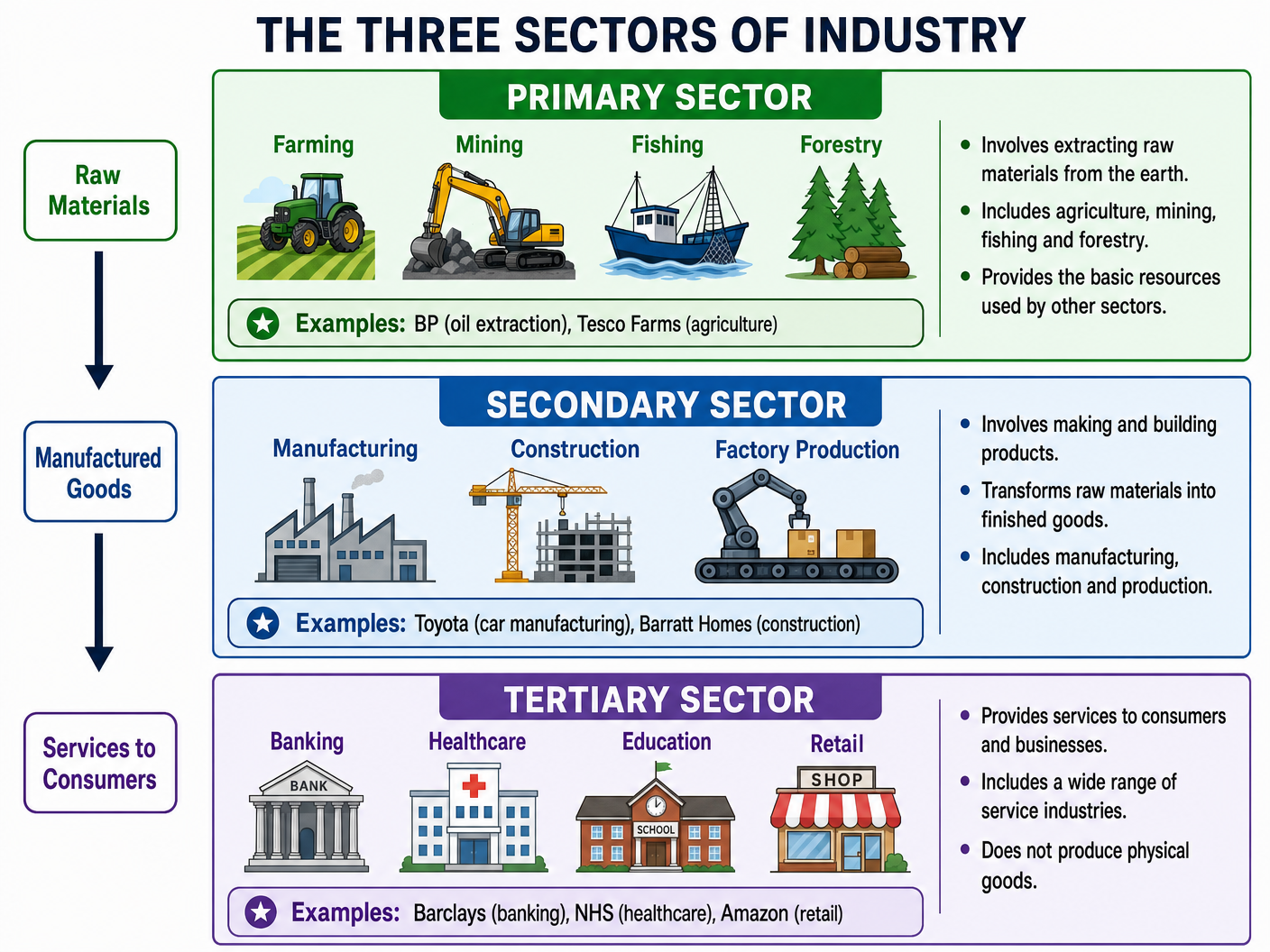

## The Three Sectors of Industry

All business activity can be categorised into three main sectors. Understanding the flow from raw materials to finished services is vital.

* **Primary Sector**: Involves extracting or harvesting raw materials from nature (e.g., farming, mining, fishing, forestry).

* **Secondary Sector**: Involves manufacturing, construction, and processing raw materials into finished goods (e.g., car manufacturing, house building).

* **Tertiary Sector**: Involves providing services to consumers and other businesses (e.g., banking, retail, healthcare, education).

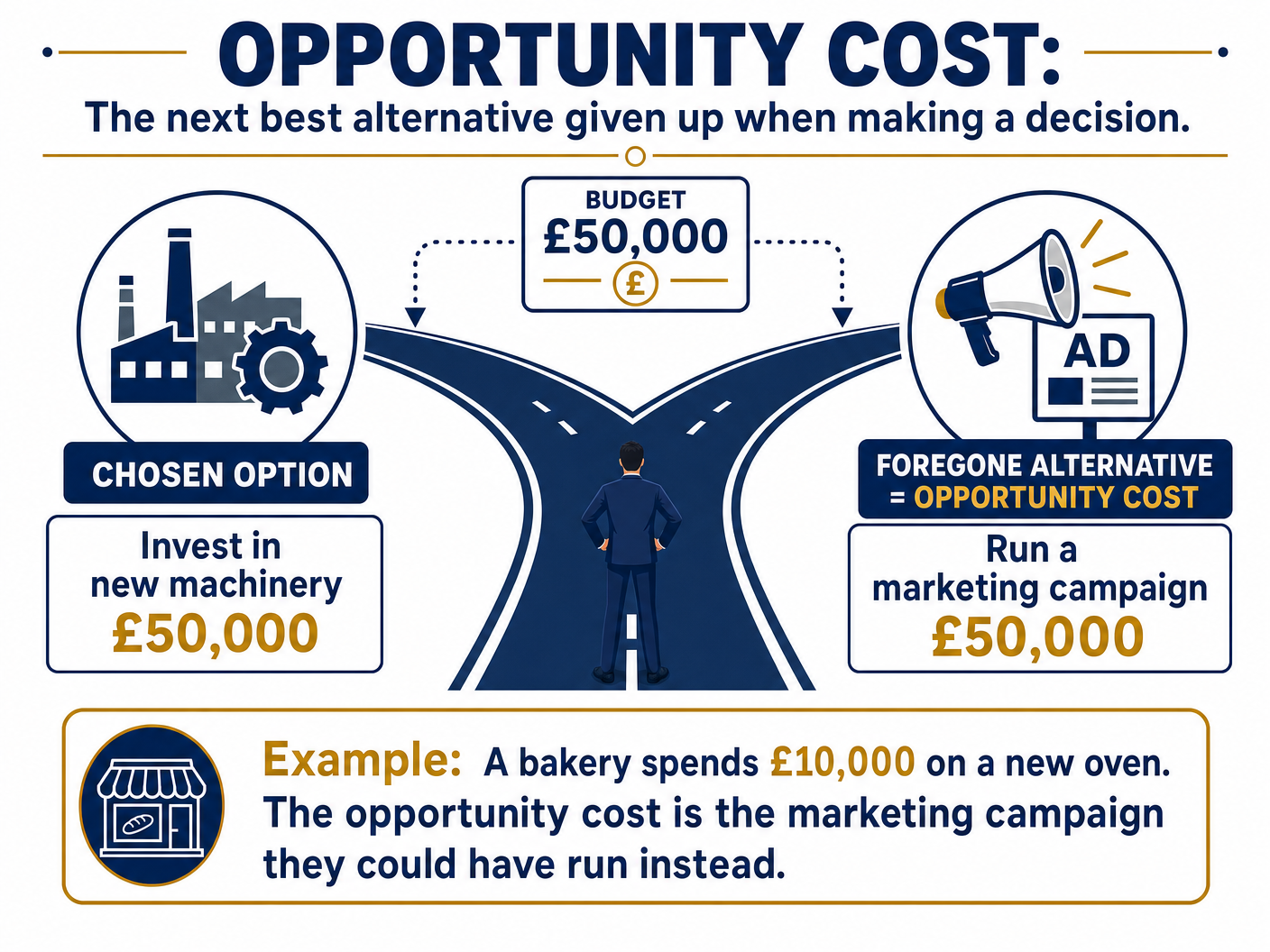

## Opportunity Cost

Opportunity cost is a fundamental economic and business concept. It is defined as **the next best alternative given up when making a decision**.

Whenever a business (or an individual) chooses to allocate resources to one option, they must sacrifice the benefits of the alternative option. For example, if a business spends £50,000 on new machinery, the opportunity cost might be the marketing campaign they could have run with that money.

## The Dynamic Business Environment

Businesses do not operate in a vacuum; they exist in a dynamic (constantly changing) environment. External factors force businesses to adapt or risk failure. These changes include:

* **Technological Change**: Advances in technology (e.g., e-commerce, automation) change how businesses produce and sell.

* **Economic Change**: Fluctuations in the economy (e.g., inflation, recession) affect consumer spending power.

* **Legal Change**: New laws and regulations (e.g., minimum wage increases, environmental standards) impact business operations.

* **Social/Environmental Change**: Shifting consumer attitudes (e.g., demand for sustainable products) require businesses to adjust their offerings.

## Podcast Summary

Listen to our comprehensive 10-minute podcast covering all the core concepts, common mistakes, and exam tips for this topic.

Key Terms & Definitions

- Business

- An organisation that exists to produce goods or supply services to satisfy customer needs and wants.

- Entrepreneur

- A person who organises the factors of production, takes financial risks, and sets up a business in the hope of making a profit.

- Factors of Production

- The resources needed to produce goods and services: Land, Labour, Capital, and Enterprise.

- Opportunity Cost

- The next best alternative given up when making a decision.

- Primary Sector

- The sector of the economy that involves the extraction or harvesting of raw materials from the earth.

- Dynamic Environment

- The constantly changing external factors (technological, economic, legal) that affect how a business operates.

Worked Examples

Worked Example

Question: Explain the difference between the primary sector and the tertiary sector, using examples. (4 marks)

Solution: **Point**: The primary sector involves the extraction of raw materials from nature, whereas the tertiary sector involves providing services to consumers or other businesses.

**Evidence**: For example, a business in the primary sector would be a coal mining company or a wheat farm.

**Explanation**: These businesses harvest the initial resources.

**Link**: In contrast, an example of a tertiary sector business is a bank like Barclays or a retailer like Tesco, which do not produce physical goods but instead offer a service to the end user.

Worked Example

Question: A local bakery has £10,000 to invest. The owner is deciding between buying a new, more efficient oven or launching a local advertising campaign. The owner decides to buy the oven. Explain the opportunity cost of this decision. (3 marks)

Solution: The opportunity cost is the next best alternative foregone when a decision is made. In this scenario, the opportunity cost of buying the new oven is the local advertising campaign that the bakery can no longer afford to run. This means the bakery gives up the potential benefit of attracting new customers that the advertising campaign might have generated.

Worked Example

Question: Discuss the importance of an entrepreneur possessing the characteristic of being a 'risk-taker'. (6 marks)

Solution: An entrepreneur is an individual who organises the factors of production to start a business, aiming to make a profit. Being a risk-taker is a crucial characteristic for an entrepreneur.

Firstly, starting a new business involves significant financial uncertainty. The entrepreneur often has to invest their own personal savings or take out loans to secure capital (such as premises or machinery) before any revenue is generated. There is no guarantee that the business will attract customers or generate enough sales to cover its costs. Therefore, without the willingness to take a calculated financial risk, the entrepreneur would never launch the business in the first place.

Furthermore, the business environment is dynamic and constantly changing due to factors like new technology or competitor actions. A risk-taking entrepreneur is more likely to innovate and try new methods or launch new products to stay ahead of the competition. While these innovations carry the risk of failure, they are essential for long-term business survival and growth. Ultimately, the willingness to take risks is the necessary catalyst for enterprise and the potential reward of profit.

Practice Questions

Question: State two factors of production. (2 marks)

Answer:

Question: Explain one reason why a person might decide to start their own business. (3 marks)

Answer:

Question: A clothing manufacturer has a budget of £20,000. They can either upgrade their sewing machines or increase the wages of their factory workers. They choose to upgrade the sewing machines. Explain the opportunity cost of this decision. (3 marks)

Answer:

Question: Discuss the impact on a high street retailer if the business environment becomes more dynamic due to rapid technological change. (6 marks)

Answer:

Question: Classify the following businesses into the correct sector of industry: A) A dairy farm, B) A car assembly plant, C) A firm of accountants. (3 marks)

Answer: