Study Notes

Overview

Finance is the lifeblood of any business. Every decision a business makes—whether it's launching a new product, hiring staff, or expanding operations—has a financial consequence. In your GCSE Business exam, examiners expect you to not only perform accurate calculations but also to interpret financial data and evaluate what it means for the business's future. This study guide covers the core concepts of revenue, costs, profit, break-even analysis, cash flow, and sources of finance.

Listen to our revision podcast to reinforce your learning:

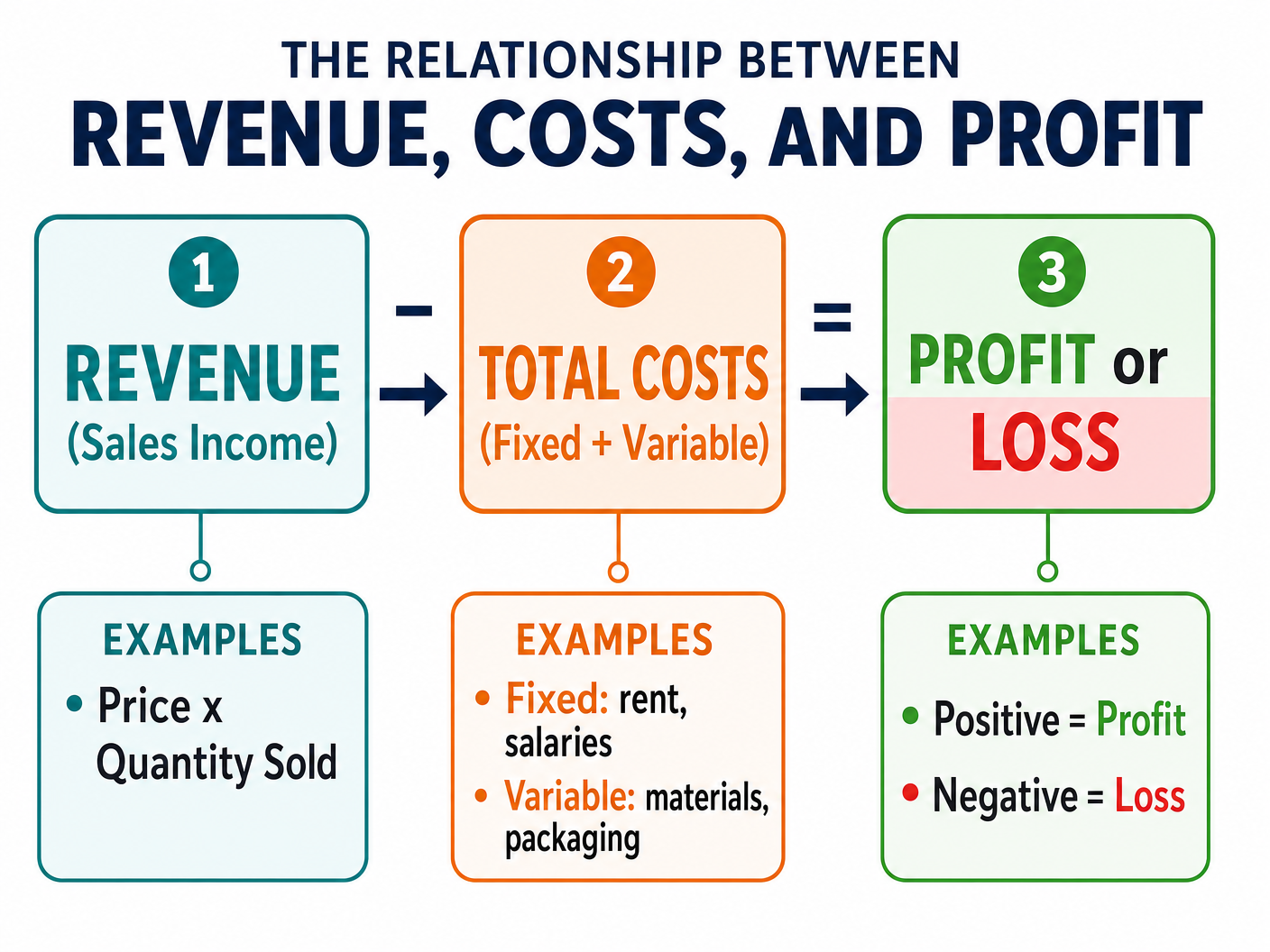

Revenue, Costs, and Profit

Understanding the relationship between money coming in and money going out is fundamental. Examiners frequently test your ability to calculate these figures and understand how changes in one affect the others.

Revenue

Definition: The total income a business earns from selling its goods or services over a given period.

Formula: Revenue = Price × Quantity Sold

Exam Focus: Candidates often lose marks by confusing revenue with profit. Revenue is just the top-line income before any costs are deducted.

Costs

Fixed Costs: Costs that do not change with the level of output (e.g., rent, insurance, salaries). They must be paid even if the business produces nothing.

Variable Costs: Costs that change directly with the level of output (e.g., raw materials, packaging, piece-rate wages).

Formula: Total Costs = Fixed Costs + Total Variable Costs

Profit

Definition: The surplus left over when total costs are deducted from total revenue. If costs exceed revenue, the business makes a loss.

Formula: Profit = Total Revenue - Total Costs

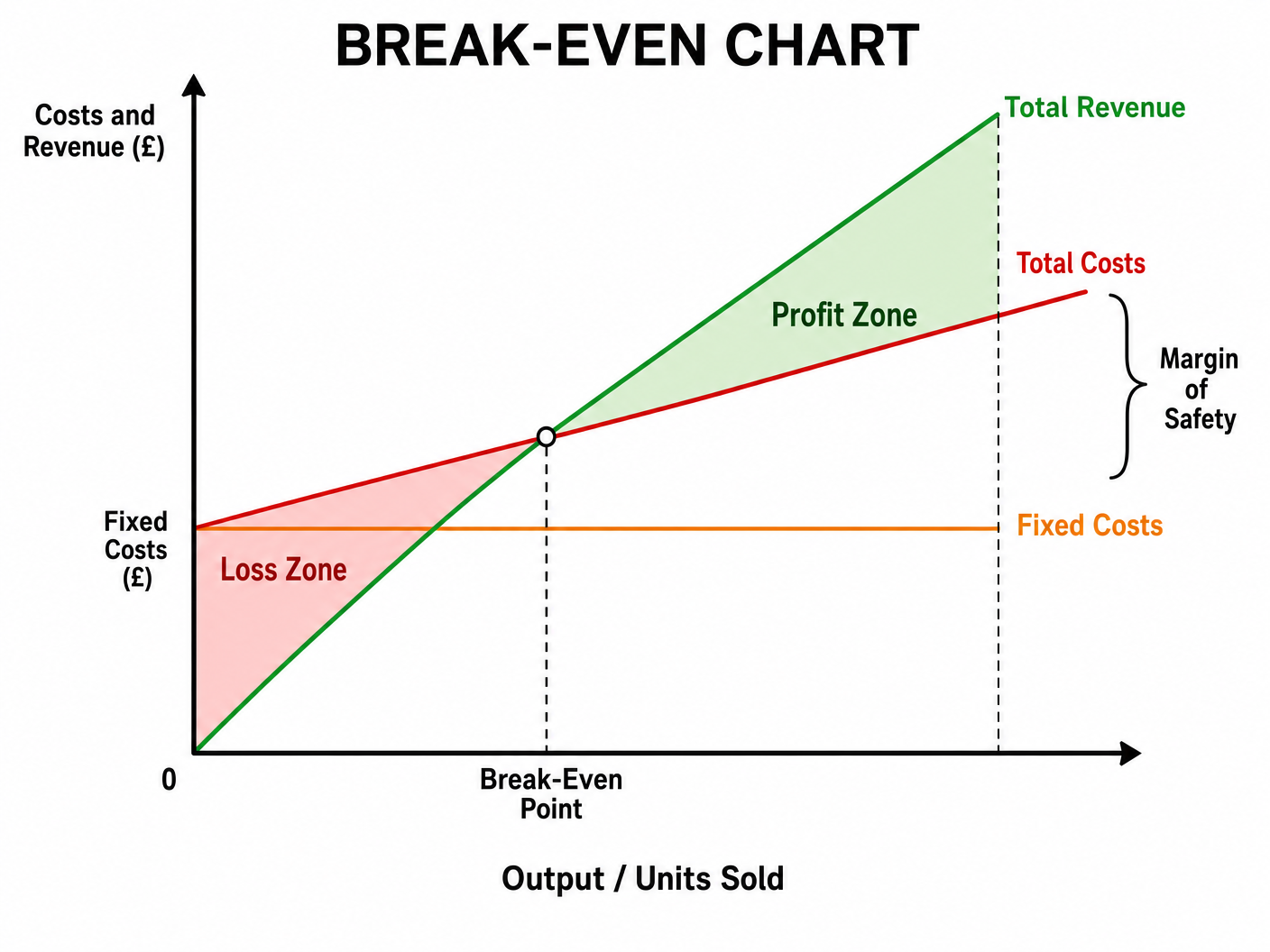

Break-Even Analysis

Break-even is a critical concept that examiners love to test through both calculations and graph interpretation.

The Break-Even Point

Definition: The level of output at which total revenue exactly equals total costs. The business is making neither a profit nor a loss.

Formula: Break-Even Point = Fixed Costs ÷ Contribution Per Unit

(Note: Contribution Per Unit = Selling Price - Variable Cost Per Unit)

Margin of Safety

Definition: The amount by which current output exceeds the break-even level of output. It shows how much sales can fall before the business starts making a loss.

Formula: Margin of Safety = Actual Output - Break-Even Output

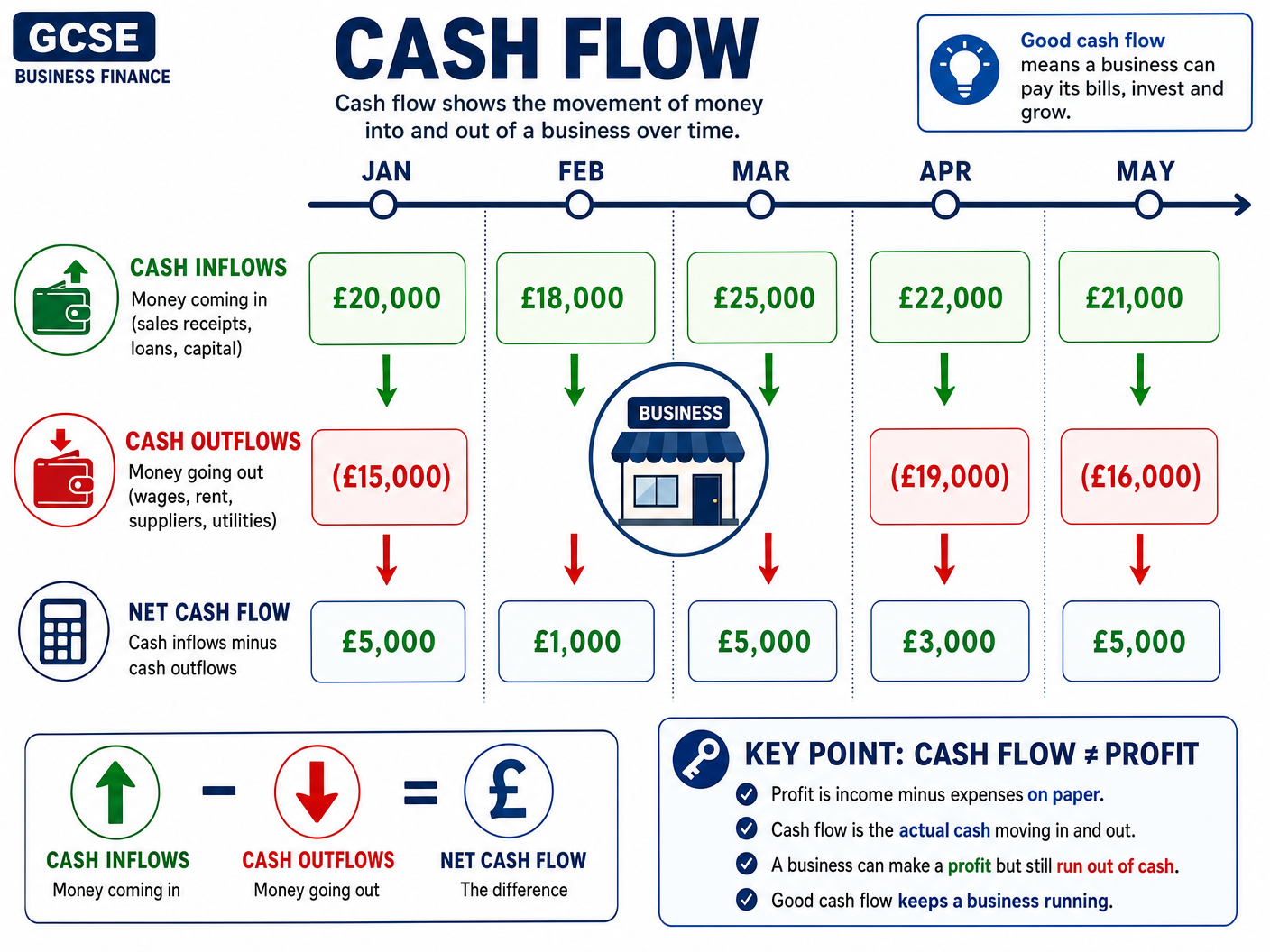

Cash Flow

Cash flow is arguably the most important day-to-day financial metric for a business. Many profitable businesses fail because they run out of cash.

Cash Flow Basics

Definition: The movement of money into and out of a business over time.

Inflows: Money coming in (e.g., cash sales, debtor payments, loans).

Outflows: Money going out (e.g., paying suppliers, wages, rent).

Formula: Net Cash Flow = Total Inflows - Total Outflows

Cash Flow Forecasts

Examiners frequently ask candidates to complete missing figures in a cash flow forecast table. Remember that the closing balance of one month always becomes the opening balance of the next month.

Sources of Finance

Businesses need capital to start up, operate, and expand. You must be able to recommend appropriate sources of finance based on the business context.

Internal Sources

- Retained Profit: Profit kept in the business after tax and dividends. Cheap, but may not be sufficient for large projects.

- Selling Assets: Raising cash by selling items the business no longer needs.

External Sources

- Bank Loan: A fixed sum borrowed and repaid with interest over a set period. Good for long-term assets.

- Overdraft: A short-term facility allowing a business to spend more than is in its bank account. High interest rates but flexible.

- Share Capital: Selling shares to investors (only for limited companies). Raises large amounts without interest payments, but dilutes ownership.

- Trade Credit: Buying goods from suppliers and paying for them later (usually 30-60 days). Excellent for short-term cash flow.

Worked Examples

3 detailed examples with solutions and examiner commentary

Practice Questions

Test your understanding — click to reveal model answers

A coffee shop has fixed costs of £2,000 per month. They sell coffee for £3.00 a cup. The variable cost per cup is £0.50. Calculate the break-even point in units. Show your workings. (3 marks)

Hint: First calculate the contribution per unit, then divide the fixed costs by that number.

Explain one impact on a business of having a negative cash flow. (3 marks)

Hint: Think about what happens if a business can't pay its bills on time.

A sole trader needs £5,000 to buy a new delivery van. Recommend whether they should use a bank loan or an overdraft. Justify your answer. (6 marks)

Hint: Consider the lifespan of the asset (the van) versus the term of the finance.

Calculate the margin of safety if a business has a break-even point of 5,000 units and is currently producing and selling 7,500 units. (2 marks)

Hint: Margin of safety is the difference between actual sales and break-even sales.

State two ways a business could improve its cash flow. (2 marks)

Hint: Think about how to get money in faster or slow money going out.