Subject: Economics | Level: GCSE | Exam Board: OCR

This study guide provides a comprehensive overview of Economic Growth for OCR GCSE Economics. It is designed to be exam-focused, helping students understand key concepts, develop analytical skills, and secure maximum marks by mastering the content and exam techniques required by examiners.

Revision Notes & Key Concepts

Revision Podcast Transcript

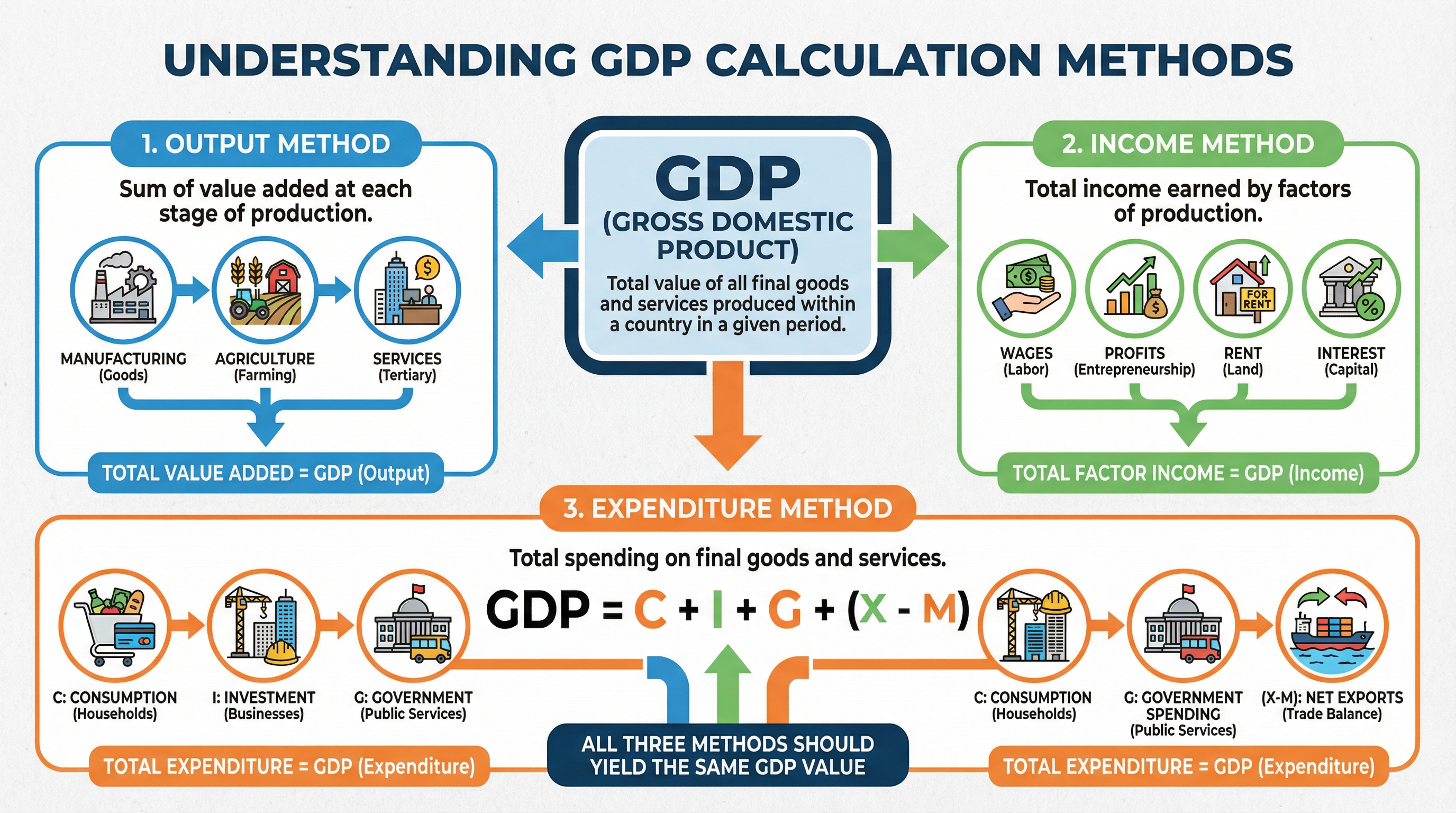

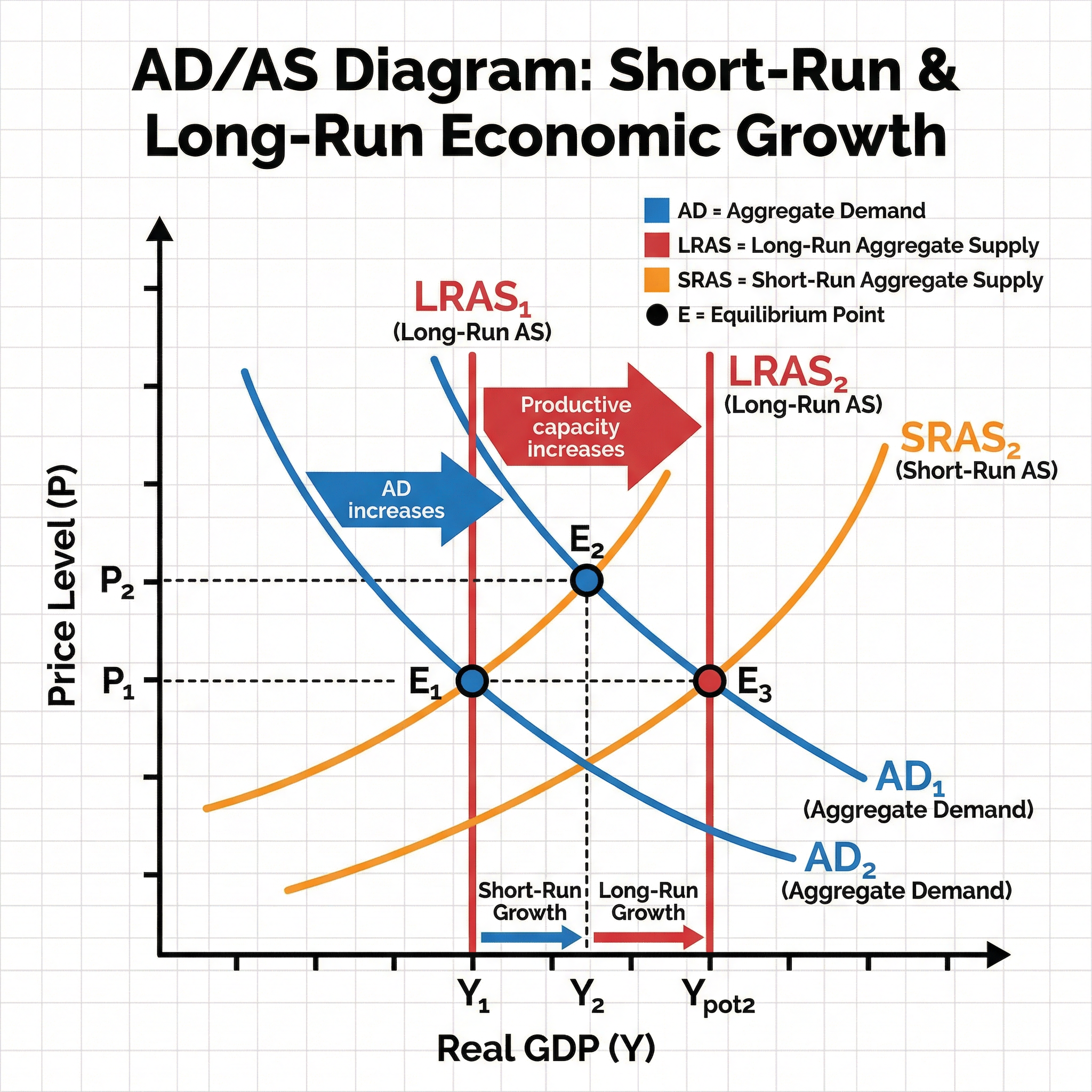

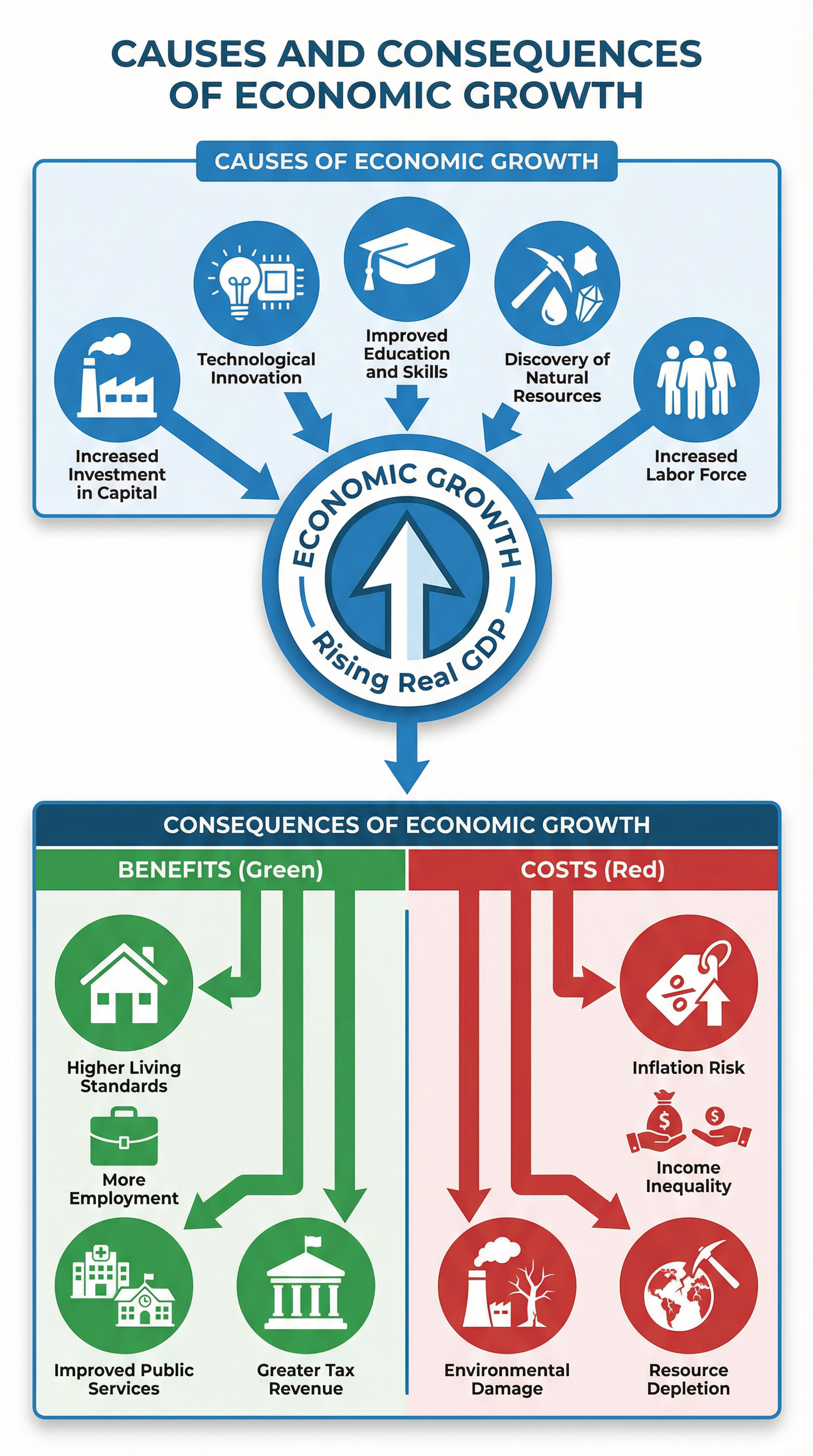

ECONOMIC GROWTH PODCAST SCRIPT - 10 MINUTES Female Voice - Warm, Conversational, Engaging Educator Tone [INTRO - 1 MINUTE] Hello and welcome to GCSE Economics Essentials! I'm your host, and today we're diving into one of the most important topics in your OCR Economics exam: Economic Growth. Now, you've probably heard politicians and news reporters talking about GDP figures and growth rates, but what does this actually mean? And more importantly, how do you answer exam questions on this topic to pick up those crucial marks? Over the next ten minutes, we're going to break down everything you need to know about economic growth. We'll cover the key definitions that examiners expect you to know word-perfect, explore what causes growth and what happens as a result, and I'll share some insider tips on how to avoid the most common mistakes that cost students marks. So grab your notes, get comfortable, and let's get started! [CORE CONCEPTS - 5 MINUTES] First things first: what exactly is economic growth? In your exam, you need to define it precisely. Economic growth is the increase in the real value of goods and services produced in an economy over time. It's measured by the percentage change in real Gross Domestic Product, or real GDP. Now, let's unpack that definition because every word matters. GDP is the total value of all final goods and services produced within a country in a given time period, usually a year. When we say "real" GDP, we mean GDP that's been adjusted for inflation. This is crucial because if prices double but output stays the same, we haven't actually grown the economy, we've just experienced inflation. Here's a key distinction that trips up a lot of students: GDP versus GDP per capita. GDP measures the total output of the economy, but GDP per capita divides that figure by the population. So if GDP grows by 3% but the population also grows by 3%, GDP per capita hasn't changed at all, which means the average person isn't any better off. Examiners love testing this distinction, so make sure you're crystal clear on when to use each measure. Now, how do we measure GDP? There are actually three different methods, and they should all give you the same answer. The output method adds up the value of all goods and services produced. The income method adds up all the incomes earned by factors of production: wages, profits, rent, and interest. And the expenditure method uses the formula C plus I plus G plus X minus M. That's consumption by households, plus investment by businesses, plus government spending, plus exports minus imports. Let's talk about what causes economic growth. In the short run, growth comes from increases in aggregate demand. That means more spending in the economy, whether it's consumers buying more, businesses investing more, the government spending more, or foreign buyers purchasing more of our exports. You'll see this on an AD-AS diagram as the aggregate demand curve shifting to the right. But here's where it gets interesting: long-run economic growth is different. Long-run growth comes from increases in productive capacity, which means the economy's ability to produce more goods and services. This happens when we increase the quantity or quality of our factors of production. Think about it: more workers, better-trained workers, more machinery, better technology, more natural resources. All of these shift the long-run aggregate supply curve to the right, increasing potential output. A really important concept here is the distinction between actual growth and potential growth. Actual growth is what's happening to real GDP right now. Potential growth is the increase in what the economy could produce if all resources were fully employed. You can have actual growth without potential growth if the economy is just using spare capacity, but sustainable long-term growth requires increases in productive capacity. Now, what are the consequences of economic growth? This is where you need to think like an economist and consider both benefits and costs. On the benefits side, economic growth typically leads to higher living standards. When real GDP per capita rises, people can afford more goods and services, which improves quality of life. Growth also tends to create more employment opportunities as businesses expand. And here's something students often forget: growth generates higher tax revenues for the government without raising tax rates, because people are earning more and spending more. That means the government can afford better public services like healthcare and education. But, and this is a big but, economic growth isn't all positive. Rapid growth can cause demand-pull inflation if aggregate demand rises faster than aggregate supply. Growth can also lead to greater income inequality if the benefits aren't distributed evenly. Some people get much richer while others are left behind. And then there are the environmental costs: more production often means more pollution, more resource depletion, and greater carbon emissions. This raises questions about sustainability. Can we keep growing forever on a planet with finite resources? [EXAM TIPS & COMMON MISTAKES - 2 MINUTES] Right, let's talk exam technique. One of the biggest mistakes students make is confusing a fall in the rate of growth with negative growth. Listen carefully: if the economy grows by 3% one year and 2% the next year, it's still growing! The rate has slowed down, but GDP is still increasing. Negative growth, which we call a recession, only happens when GDP actually falls. Another common error is forgetting to adjust for population when discussing living standards. If the question asks about living standards or quality of life, you must use GDP per capita, not just GDP. Examiners will not give you full marks if you ignore this distinction. When you're answering calculation questions, always show your working. The mark scheme often awards marks for method even if your final answer is wrong. For percentage change, the formula is: new value minus old value, divided by old value, times 100. Write it out clearly. For longer analysis and evaluation questions, remember your assessment objectives. AO1 is knowledge: define your terms precisely. AO2 is application: use the context from the question. AO3 is analysis: explain cause and effect with logical chains of reasoning. Use phrases like "this leads to" and "as a result" to show you're analyzing, not just describing. And here's a top tip for evaluation questions: always consider trade-offs. Economic growth might increase living standards, but it might also increase inequality or environmental damage. The best answers weigh up these competing factors and reach a supported judgment. Don't just list points; compare them and say which matters more in the specific context of the question. [QUICK-FIRE RECALL QUIZ - 1 MINUTE] Okay, let's test your knowledge with a quick-fire recall quiz. I'll ask a question, pause for a moment, then give you the answer. Question 1: What does GDP stand for? [Pause] Answer: Gross Domestic Product. Question 2: What's the difference between real GDP and nominal GDP? [Pause] Answer: Real GDP is adjusted for inflation; nominal GDP is not. Question 3: What formula represents the expenditure method of calculating GDP? [Pause] Answer: C plus I plus G plus X minus M. Question 4: What shifts the long-run aggregate supply curve to the right? [Pause] Answer: Increases in the quantity or quality of factors of production. Question 5: Name two benefits and two costs of economic growth. [Pause] Answer: Benefits: higher living standards, more employment. Costs: inflation, environmental damage. How did you do? If you got them all, brilliant! If not, go back and review those concepts. [SUMMARY & SIGN-OFF - 1 MINUTE] Let's wrap up. Today we've covered the essential knowledge you need for economic growth: the precise definitions of GDP and real GDP, the three methods of measuring GDP, the distinction between short-run and long-run growth, and the causes and consequences of growth including both benefits and costs. Remember, in your exam, examiners are looking for precise economic terminology, clear chains of reasoning, and balanced evaluation that considers trade-offs. Always adjust for population when discussing living standards, always show your working in calculations, and always link your analysis back to the specific context in the question. Economic growth is a core topic in OCR GCSE Economics, and it links to so many other areas: inflation, unemployment, government policy, international trade. Master this topic, and you'll find the rest of the course much easier to understand. Thanks for listening to GCSE Economics Essentials. Keep practicing those exam questions, and I'll see you next time. Good luck with your revision!

Key Terms & Definitions

- Economic Growth

- The increase in the real value of goods and services produced in an economy over time, measured by the percentage change in real GDP.

- Gross Domestic Product (GDP)

- The total value of all final goods and services produced within a country in a given time period.

- Real GDP

- GDP adjusted for inflation. It measures the actual volume of output.

- GDP per Capita

- Total GDP divided by the population. It is a measure of the average income per person.

- Recession

- A period of negative economic growth, technically defined as two consecutive quarters of falling real GDP.

- Productive Potential

- The maximum output that an economy can produce if all its resources are fully and efficiently employed.

Worked Examples

Worked Example

Question: Analyse how an increase in investment could lead to economic growth. (6 marks)

Solution: **Introduction**: An increase in investment, which is spending by firms on capital goods, can lead to both short-run and long-run economic growth. **Chain of Reasoning 1 - Short-Run Growth**: Investment (I) is a component of Aggregate Demand (AD), where AD = C + I + G + (X-M). Therefore, a direct increase in investment will cause the AD curve to shift to the right. This leads to an increase in real GDP, representing short-run economic growth, as the economy moves to a new equilibrium at a higher level of output. **Chain of Reasoning 2 - Long-Run Growth**: Investment in new machinery, technology, and infrastructure increases the economy's stock of capital goods. This improves the quality and quantity of the factors of production, leading to an increase in the productive potential of the economy. As a result, the Long-Run Aggregate Supply (LRAS) curve shifts to the right, signifying long-run economic growth.

Worked Example

Question: Evaluate whether economic growth always increases living standards. (12 marks)

Solution: **Introduction**: Economic growth, defined as an increase in real GDP, is often associated with rising living standards. However, the relationship is not always straightforward, and there are several reasons why growth may not translate into a better quality of life for the average person. **Argument For - Growth Increases Living Standards**: Economic growth typically leads to higher real GDP per capita, meaning average incomes rise. This allows households to purchase more goods and services, satisfying more of their wants and needs. Furthermore, growth creates employment opportunities, reducing unemployment and poverty. The resulting fiscal dividend for the government (higher tax revenue) can also be used to improve public services like healthcare and education, further enhancing the quality of life. **Argument Against - Growth Does Not Always Increase Living Standards**: Firstly, if population growth outpaces GDP growth, GDP per capita will fall, and living standards could decline. Secondly, the benefits of growth may not be distributed evenly. If growth leads to rising income inequality, a small portion of the population may see their incomes rise significantly while the majority see little or no improvement. Thirdly, growth can have significant negative externalities. For example, increased industrial production may lead to air and water pollution, which can harm health and reduce well-being. Finally, the composition of GDP matters; an increase in defence spending, for instance, contributes to GDP but does not directly improve the average citizen's living standards. **Conclusion**: In conclusion, while economic growth has the potential to significantly increase living standards, it does not do so automatically. The extent to which growth benefits the population depends on how the gains are distributed, the impact on the environment, and changes in the population. Therefore, a government aiming to improve living standards must not only pursue growth but also implement policies to ensure that growth is sustainable and inclusive.

Worked Example

Question: Calculate the percentage change in Real GDP if Nominal GDP increased from £2,000bn to £2,100bn, and the price level increased by 2%. (4 marks)

Solution: **Step 1: Calculate the percentage change in Nominal GDP.** Percentage Change = ((New Value - Old Value) / Old Value) * 100 = ((£2,100bn - £2,000bn) / £2,000bn) * 100 = (£100bn / £2,000bn) * 100 = 5% **Step 2: Calculate the percentage change in Real GDP.** Real GDP Growth = Nominal GDP Growth - Inflation Rate = 5% - 2% = 3% **Answer**: Real GDP increased by 3%.

Practice Questions

Question: Explain two potential causes of long-run economic growth. (6 marks)

Answer:

Question: Analyse the impact of a significant fall in consumer confidence on economic growth. (6 marks)

Answer:

Question: Evaluate the view that economic growth is always beneficial for an economy. (12 marks)

Answer:

Question: A country's GDP is £500bn and its population is 50 million. Calculate the GDP per capita. (2 marks)

Answer:

Question: Explain the difference between actual growth and potential growth. (4 marks)

Answer: