Study Notes

Overview

Economic growth signifies an expansion in the productive capacity of an economy, measured by the increase in Real Gross Domestic Product (GDP). For WJEC examiners, a thorough understanding of this topic is non-negotiable. It requires candidates to not only define and measure growth but also to critically evaluate its wide-ranging consequences. This involves analysing the distinction between short-run growth, driven by aggregate demand, and long-run growth, underpinned by improvements in aggregate supply. A high-level response will demonstrate a clear grasp of the trade-offs involved, particularly the conflict between rising incomes and environmental sustainability. This guide will equip you with the precise definitions, analytical frameworks, and evaluative skills needed to deconstruct any question on economic growth and construct a mark-maximising answer.

Measuring Economic Growth

Gross Domestic Product (GDP)

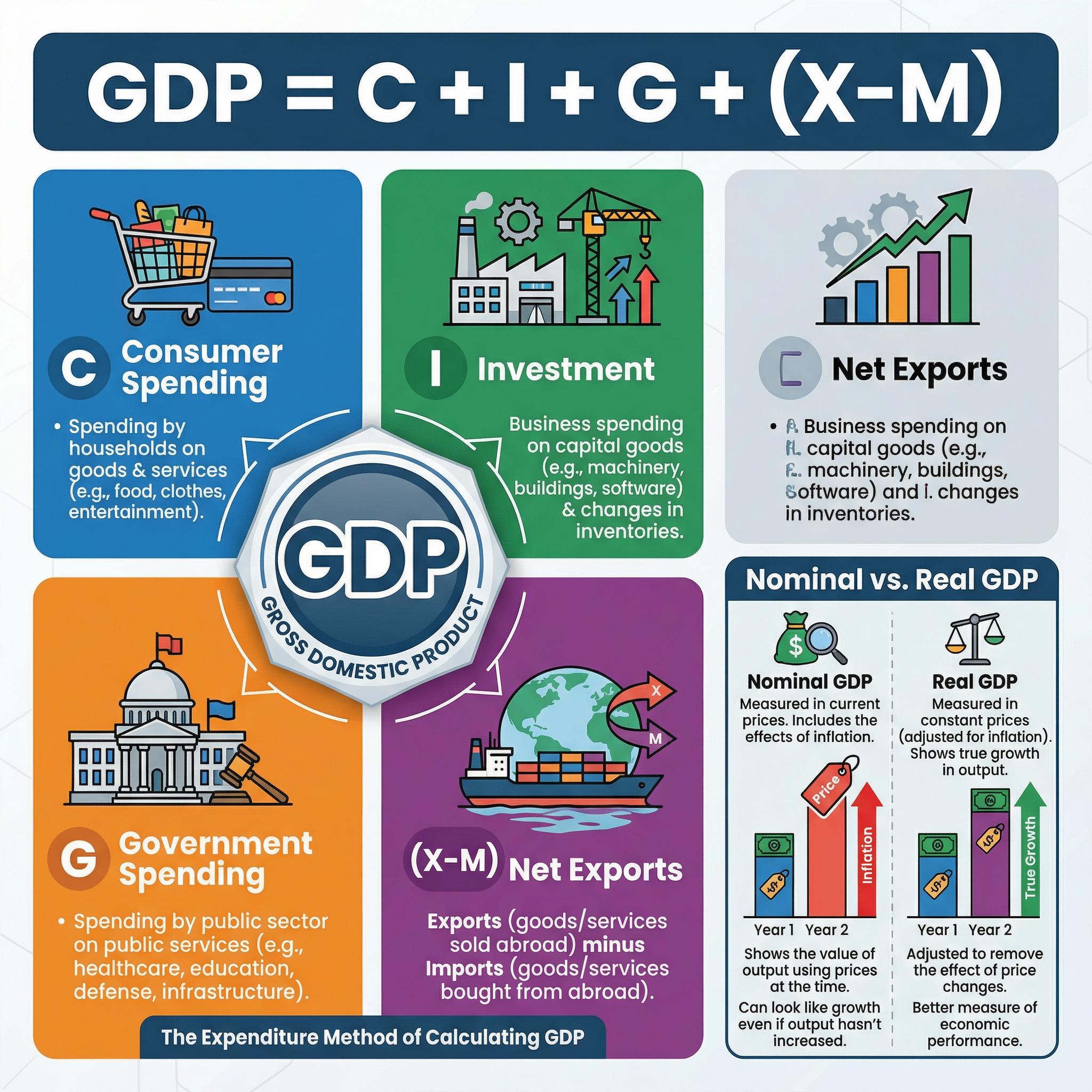

What it is: GDP is the total monetary value of all finished goods and services produced within a country's borders in a specific time period. It is the primary measure of a country's economic output.

Why it matters: Examiners expect you to know that a rise in Real GDP indicates economic growth. You must be able to distinguish between Nominal GDP, which is measured at current market prices and includes inflation, and Real GDP, which is adjusted for inflation to reflect the true change in output. Credit is consistently given for this distinction.

Specific Knowledge: The formula for calculating GDP via the expenditure method is GDP = C + I + G + (X-M), where:

- C = Consumer Spending

- I = Investment

- G = Government Spending

- (X-M) = Net Exports (Exports minus Imports)

Causes of Economic Growth

Short-Run vs. Long-Run Growth

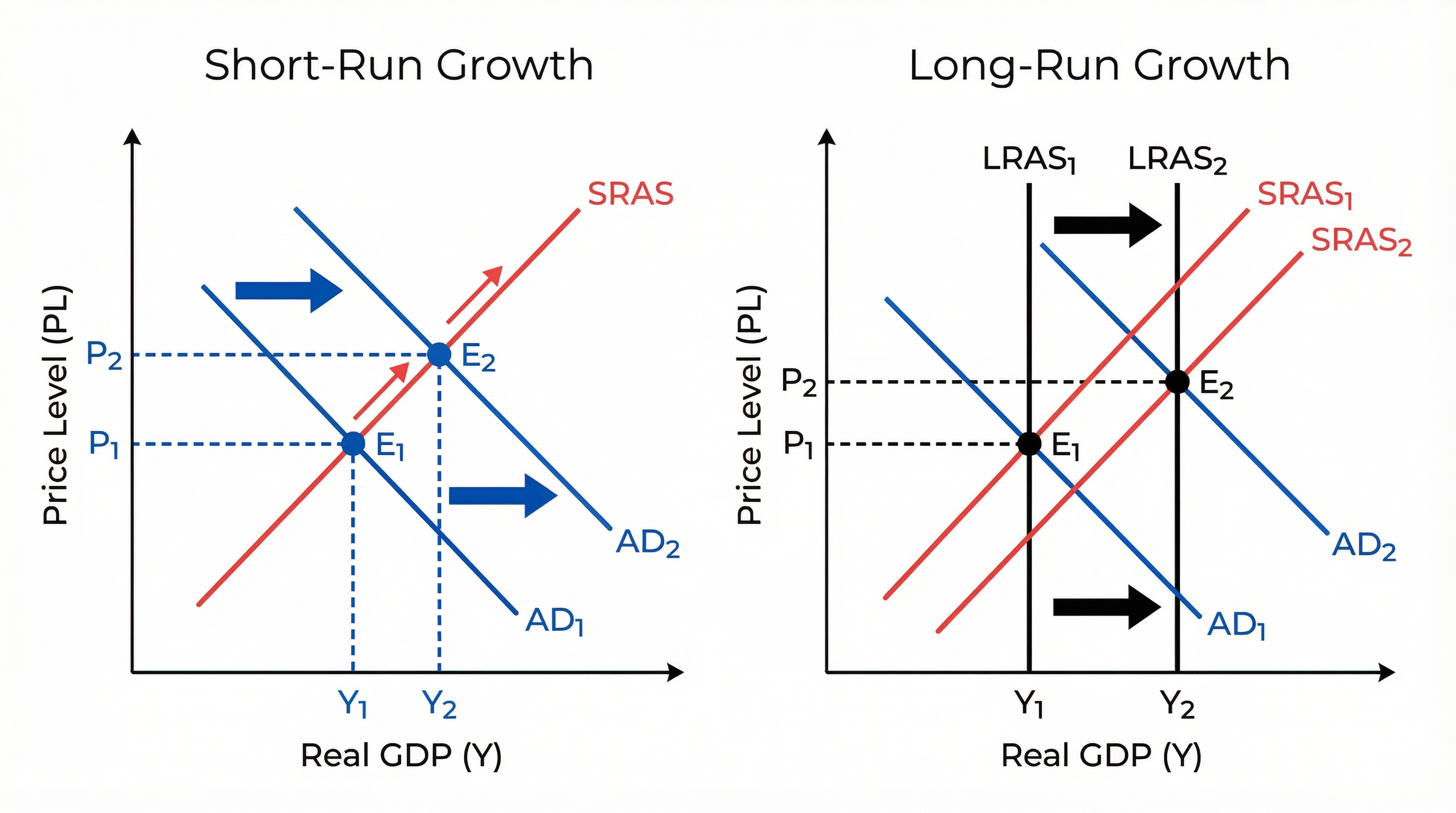

Understanding the difference between short-run and long-run growth is essential for achieving higher marks. Examiners look for candidates who can illustrate these concepts using the Aggregate Demand/Aggregate Supply (AD/AS) model.

Short-Run Growth: This is caused by an increase in Aggregate Demand (AD). When consumers, businesses, or the government spend more, or when net exports rise, the AD curve shifts to the right. This leads to an increase in Real GDP, but as the economy moves up the Short-Run Aggregate Supply (SRAS) curve, it can also lead to demand-pull inflation.

Long-Run Growth: This is more sustainable and is caused by an increase in the economy's productive potential, represented by a rightward shift in the Long-Run Aggregate Supply (LRAS) curve. This is driven by supply-side factors such as:

- Increased Investment: Spending on new capital goods (machinery, technology) boosts productivity.

- Technological Progress: Innovation allows more output to be produced from the same inputs.

- Improvements in Human Capital: A more educated and skilled workforce is more productive.

- Infrastructure Development: Better transport and communication networks reduce business costs.

Consequences of Economic Growth

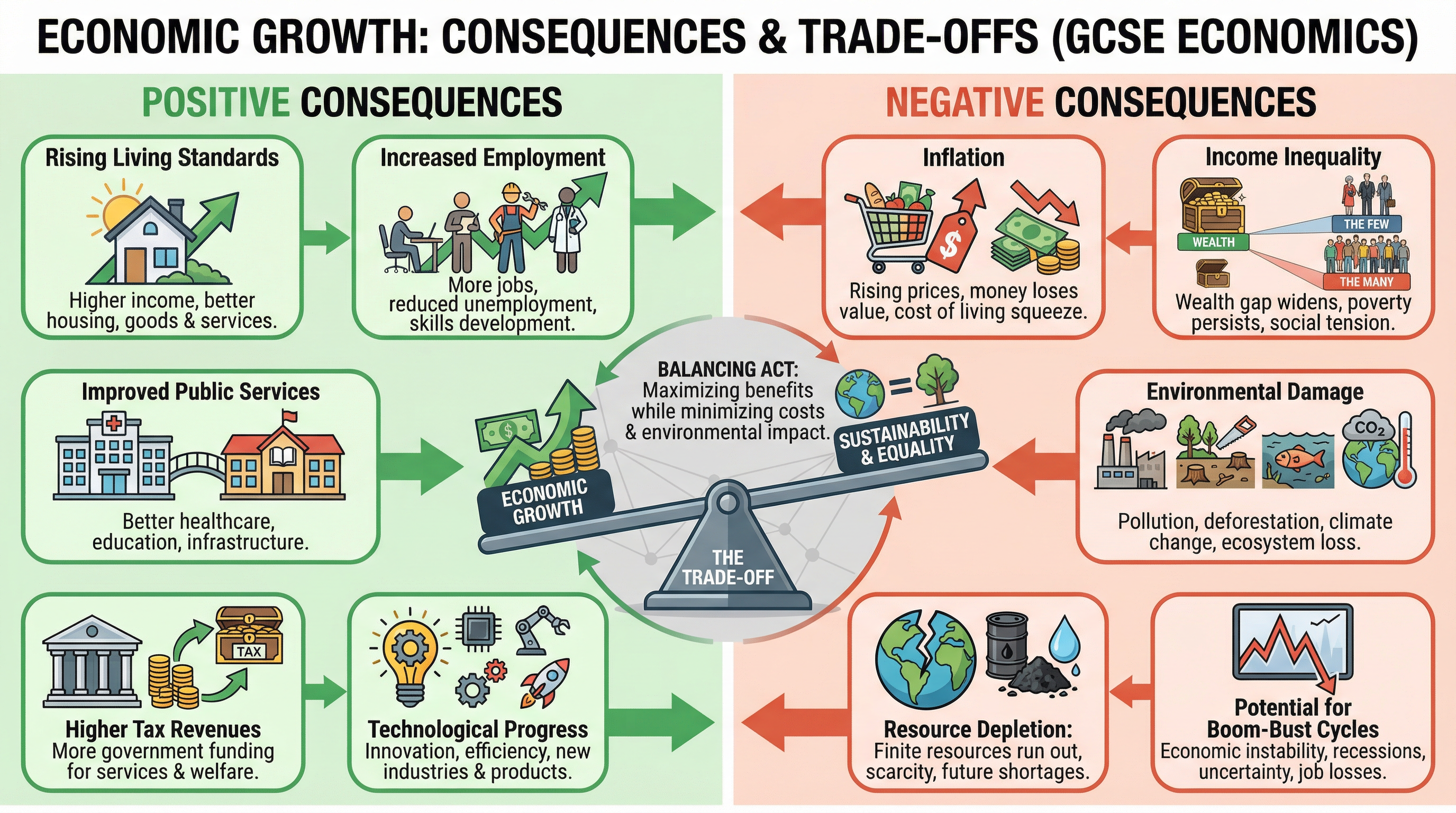

This is a prime area for evaluation questions. You must be able to analyse both the benefits and the costs of economic growth.

Positive Consequences

- Rising Living Standards: Higher GDP per capita generally means higher average incomes, allowing people to afford more goods and services, better housing, and improved nutrition.

- Increased Employment: As businesses expand production, they need to hire more workers, leading to lower unemployment.

- Improved Public Services: Economic growth generates a 'fiscal dividend'. As incomes and profits rise, the government collects more tax revenue, which can be used to fund better healthcare, education, and infrastructure.

- Technological Innovation: Growth incentivises firms to invest in research and development, leading to new products and more efficient production processes.

Negative Consequences

- Inflation: If aggregate demand grows faster than aggregate supply, it can lead to demand-pull inflation, eroding the purchasing power of money.

- Income and Wealth Inequality: The benefits of growth are not always shared equally. Those with assets and high skills may see their incomes rise significantly, while low-skilled workers may be left behind, widening the gap between rich and poor.

- Environmental Damage: This is a key trade-off. Increased production often leads to negative externalities such as pollution, carbon emissions, deforestation, and the depletion of non-renewable resources. Examiners will credit candidates who can evaluate the conflict between economic growth and environmental sustainability.

- Boom and Bust Cycles: Rapid, unsustainable growth can lead to economic instability, creating inflationary booms followed by recessions and job losses.