Government Intervention (Taxes, Subsidies, Price Controls) — OCR GCSE Study Guide

Exam Board: OCR | Level: GCSE

This study guide provides a comprehensive overview of government intervention in markets for the OCR GCSE Economics exam. It covers the essential concepts of indirect taxes, subsidies, and price controls, focusing on the analytical and evaluative skills required to achieve top marks.

## Overview

Government intervention is a core topic in economics, exploring how and why governments step in to influence market outcomes. For your OCR GCSE Economics exam, you are expected to master the analysis of three main tools: indirect taxes, subsidies, and price controls (both maximum and minimum prices). This involves not just understanding the theory but also being able to illustrate these concepts using supply and demand diagrams, analyse their impact on consumers, producers, and the government, and critically evaluate their effectiveness. Examiners will award significant credit for candidates who can use the concept of price elasticity of demand (PED) to judge the real-world impact of these interventions. This guide will equip you with the knowledge, analytical skills, and exam technique to confidently tackle questions on this fundamental topic.

## Key Concepts & Developments

### Indirect Taxes

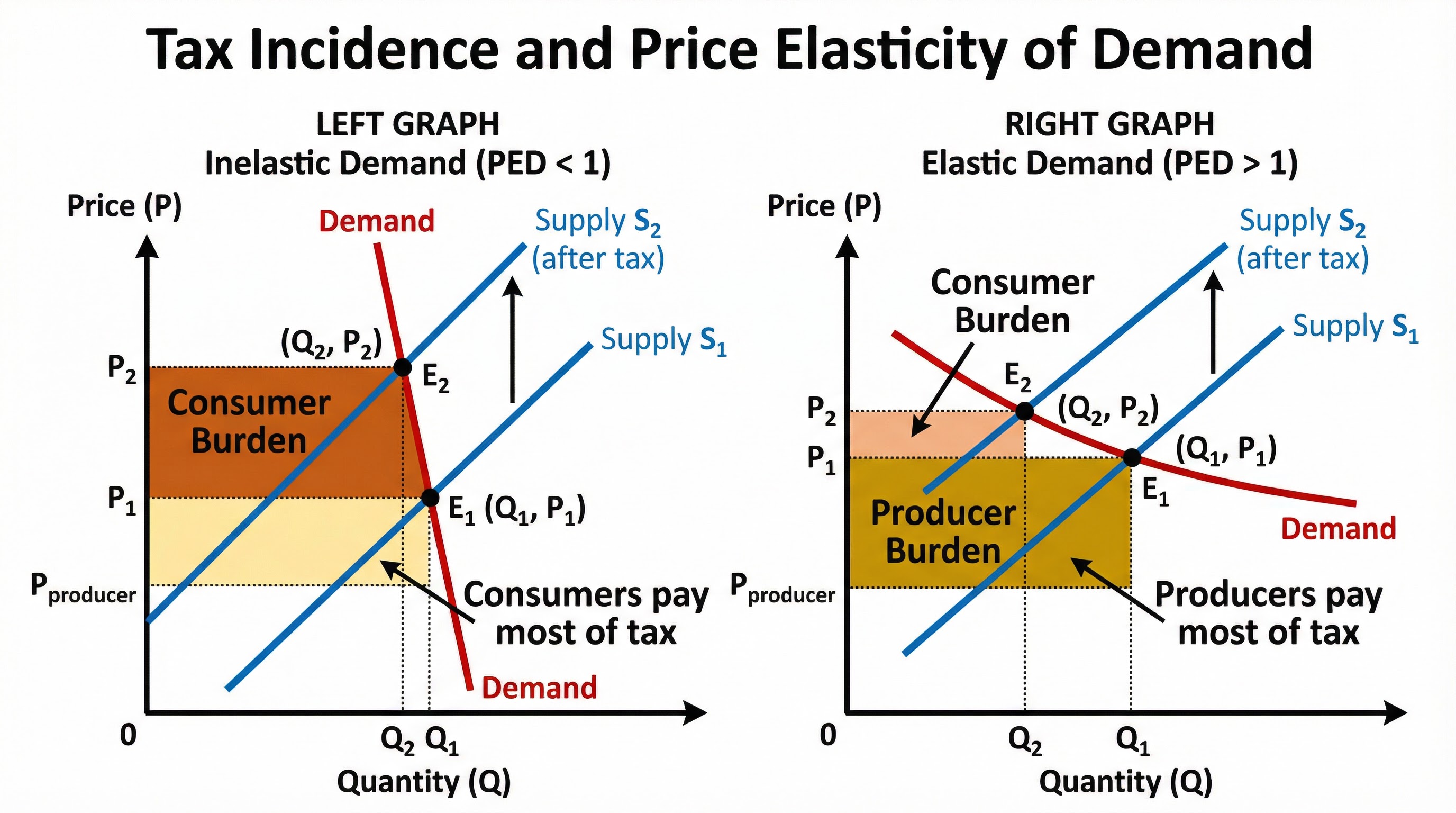

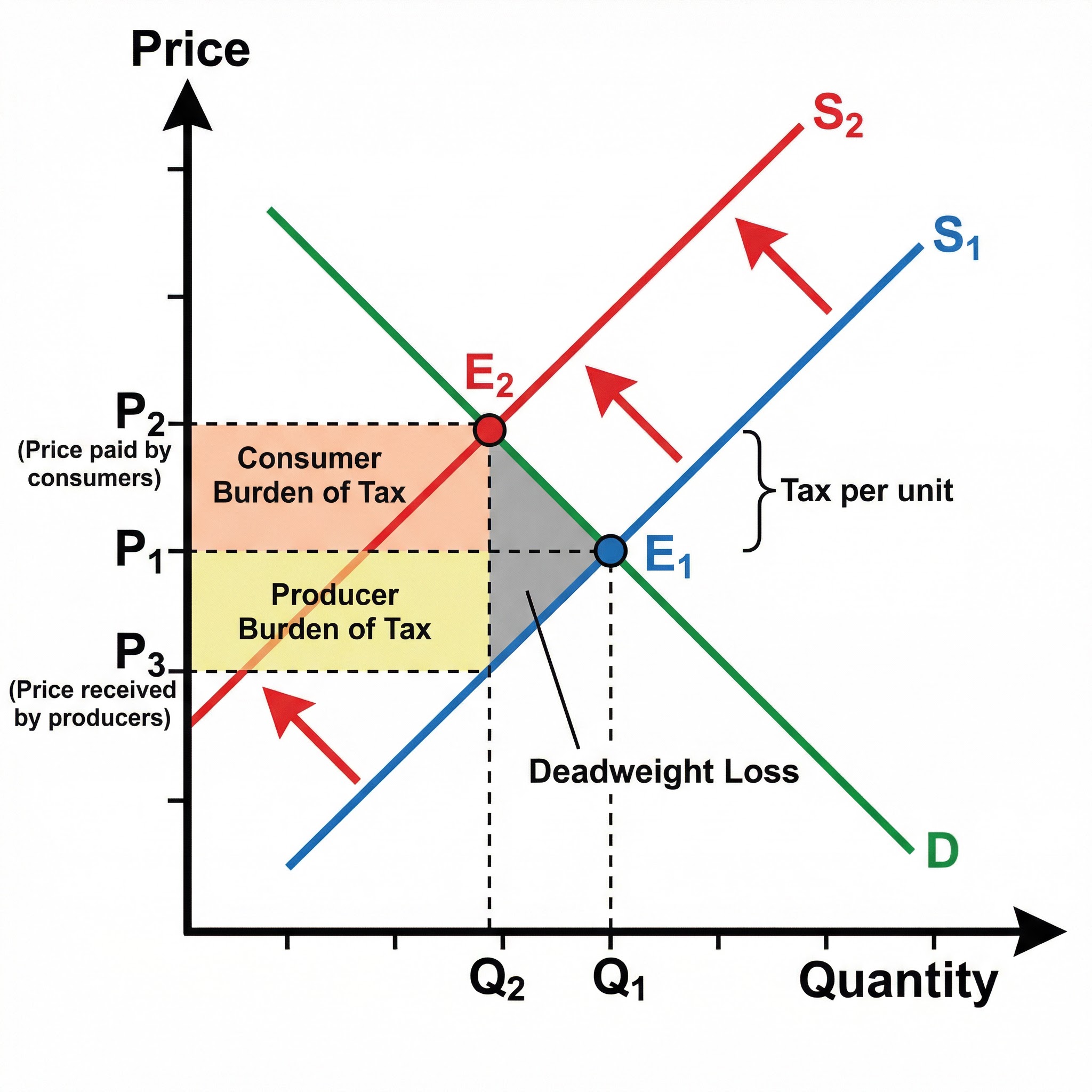

**What they are**: An indirect tax is a tax imposed by the government on spending. This increases the cost of production for firms, leading to a decrease in supply. Examples include Value Added Tax (VAT) and excise duties on fuel, alcohol, and tobacco.

**Why it matters**: Governments use indirect taxes to raise revenue and to discourage the consumption of demerit goods (goods with negative externalities, like cigarettes). Your exam will require you to show this by shifting the supply curve to the left. The key to high-level analysis is understanding how the price elasticity of demand determines who ultimately pays the tax.

**Specific Knowledge**: You must be able to draw a diagram showing the supply curve shifting left from S1 to S2. The vertical distance between the two supply curves represents the tax per unit. You should be able to identify the new equilibrium price (P2) and quantity (Q2), the total tax revenue for the government (tax per unit x Q2), and the separate burdens on the consumer and producer.

### Subsidies

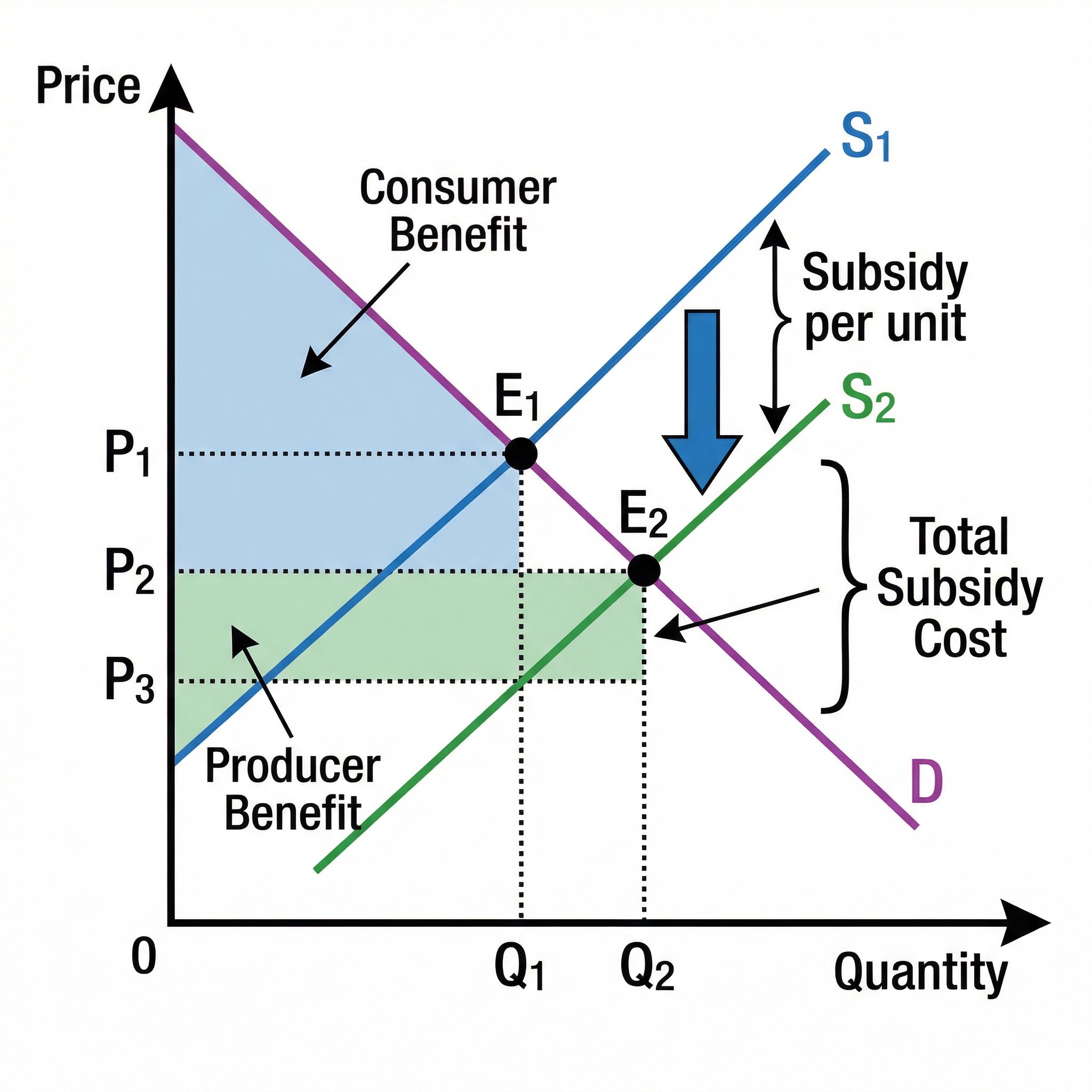

**What they are**: A subsidy is a grant or payment from the government to producers to encourage the production of a good or service, often a merit good (like education or healthcare). This lowers the cost of production.

**Why it matters**: Subsidies are used to increase the consumption of merit goods by lowering their price. They can also be used to support key industries or promote positive externalities, such as subsidies for renewable energy. In the exam, you must shift the supply curve to the right.

**Specific Knowledge**: Your diagram should show the supply curve shifting right from S1 to S2. This leads to a lower market price (P2) and a higher quantity (Q2). You need to be able to identify the consumer benefit (the price fall) and the producer benefit. The total cost of the subsidy to the government is the subsidy per unit multiplied by the new quantity (Q2).

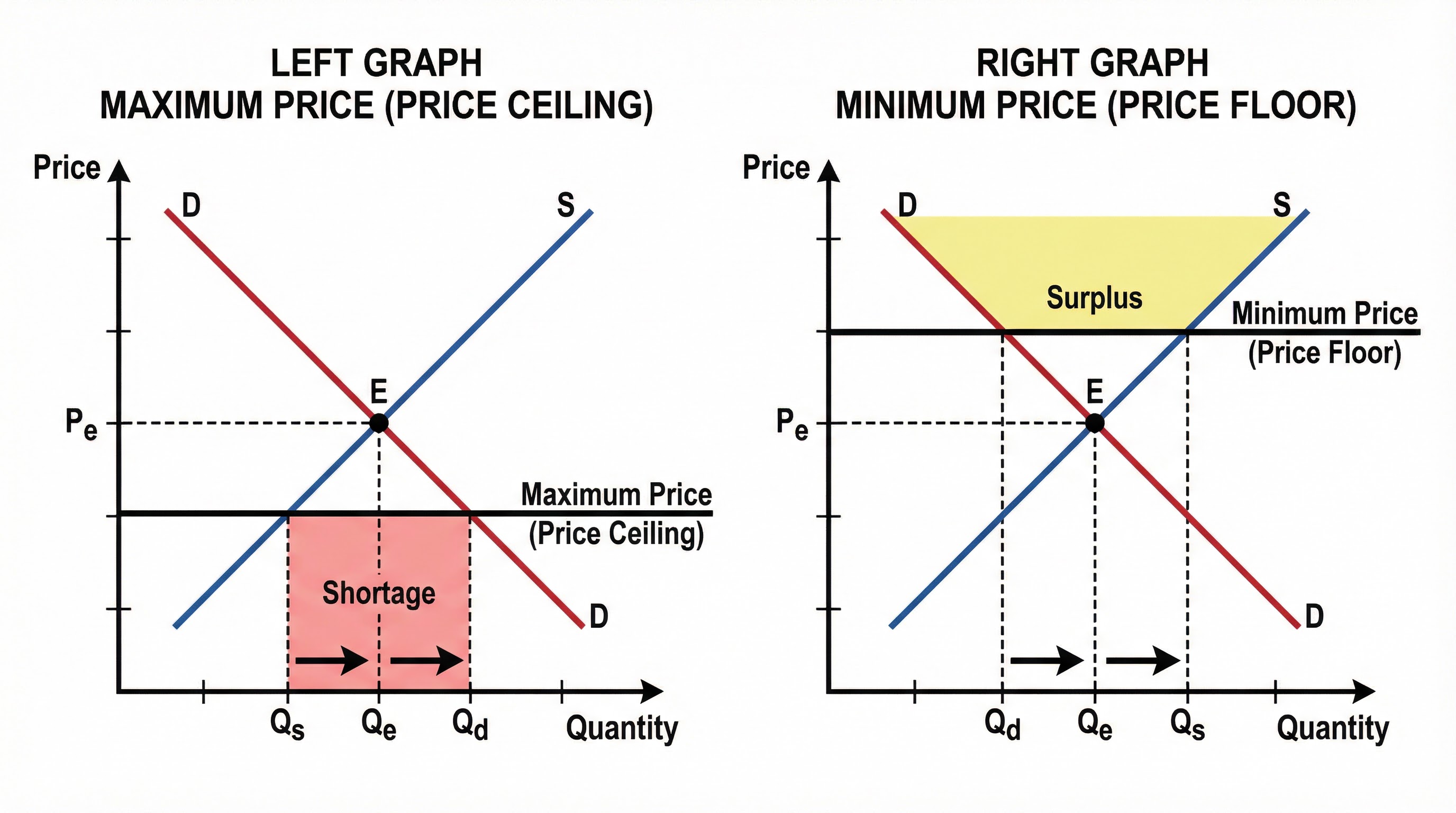

### Price Controls

**What they are**: Price controls are limits on the prices that can be charged for goods and services. There are two types: maximum prices (price ceilings) and minimum prices (price floors).

**Why it matters**: Maximum prices are set to make essential goods more affordable, but they can lead to shortages. Minimum prices are set to protect producers' incomes or ensure a minimum wage for workers, but they can lead to surpluses.

**Specific Knowledge**: For a **maximum price**, you must draw a horizontal line below the equilibrium price, showing that quantity demanded (Qd) exceeds quantity supplied (Qs), creating a shortage. For a **minimum price**, you must draw a horizontal line above the equilibrium price, showing that quantity supplied (Qs) exceeds quantity demanded (Qd), creating a surplus.

## Second-Order Concepts

### Causation

- **Market Failure**: Government intervention is often a response to market failure, such as the over-consumption of demerit goods or the under-provision of merit goods.

- **Equity**: Interventions like maximum prices on rent aim to create a fairer distribution of resources.

### Consequence

- **Intended Consequences**: Taxes raise revenue and reduce consumption; subsidies lower prices and increase consumption.

- **Unintended Consequences**: Taxes can create black markets. Subsidies can be very costly and lead to inefficiency. Maximum prices cause shortages and queues. Minimum prices cause surpluses and can lead to unemployment.

### Significance

- The significance of any intervention depends heavily on the **price elasticity of demand and supply**. This concept is your key to evaluation and achieving the highest marks. For example, a tax on a good with inelastic demand will be very effective at raising revenue but ineffective at reducing consumption.