Scarcity and Opportunity Cost — OCR GCSE Study Guide

Exam Board: OCR | Level: GCSE

This guide explores the core economic problem of scarcity—the conflict between our unlimited wants and the world's limited resources. It unpacks the crucial concept of opportunity cost, the true cost of every decision, providing a foundational understanding essential for any aspiring economist and for securing top marks in the OCR GCSE exam.

## Overview

The fundamental economic problem is the central issue in economics: how to allocate scarce resources to satisfy infinite human wants. For the OCR J205 specification, candidates must not only understand this concept but also be able to apply it to various economic agents, including consumers, producers, and the government. Examiners expect a clear understanding of how scarcity necessitates choice, which in turn leads to an opportunity cost. This guide will break down these core principles, providing you with the analytical tools and specific knowledge required to demonstrate a sophisticated understanding. A key focus will be on the Factors of Production and their rewards, a frequent topic in examination questions. Mastery of this topic is not just about memorising definitions; it is about constructing logical chains of reasoning to analyse the consequences of economic decisions.

## The Fundamental Economic Problem

### Scarcity: The Core Concept

**What it is**: Scarcity is the permanent condition where there are insufficient resources to meet all of the wants of economic agents. It is the starting point for all of economics. It is crucial to distinguish scarcity from a shortage, which is a temporary situation where demand exceeds supply in a specific market.

**Why it matters**: Because of scarcity, choices must be made. No one can have everything. This applies to individuals with limited incomes, businesses with limited budgets, and governments with limited tax revenues. Every decision to use a resource in one way is a decision not to use it in another.

**Specific Knowledge**: You must be able to state that wants are **infinite** while resources are **finite**.

### Choice and Opportunity Cost

**What it is**: When a choice is made, an alternative is always foregone. The **opportunity cost** is the value of the **next best alternative foregone**. This is a non-negotiable definition for the exam. For example, if a government chooses to spend £1 billion on a new hospital, and the next best alternative use of that money was to build 100 new schools, then the 100 schools represent the opportunity cost.

**Why it matters**: Opportunity cost reveals the true cost of a decision. The financial cost of the hospital is £1 billion, but the opportunity cost is the loss of potential educational benefits from the schools. Examiners will award significant credit for candidates who can distinguish between these two and analyse the full implications of a choice.

## Factors of Production

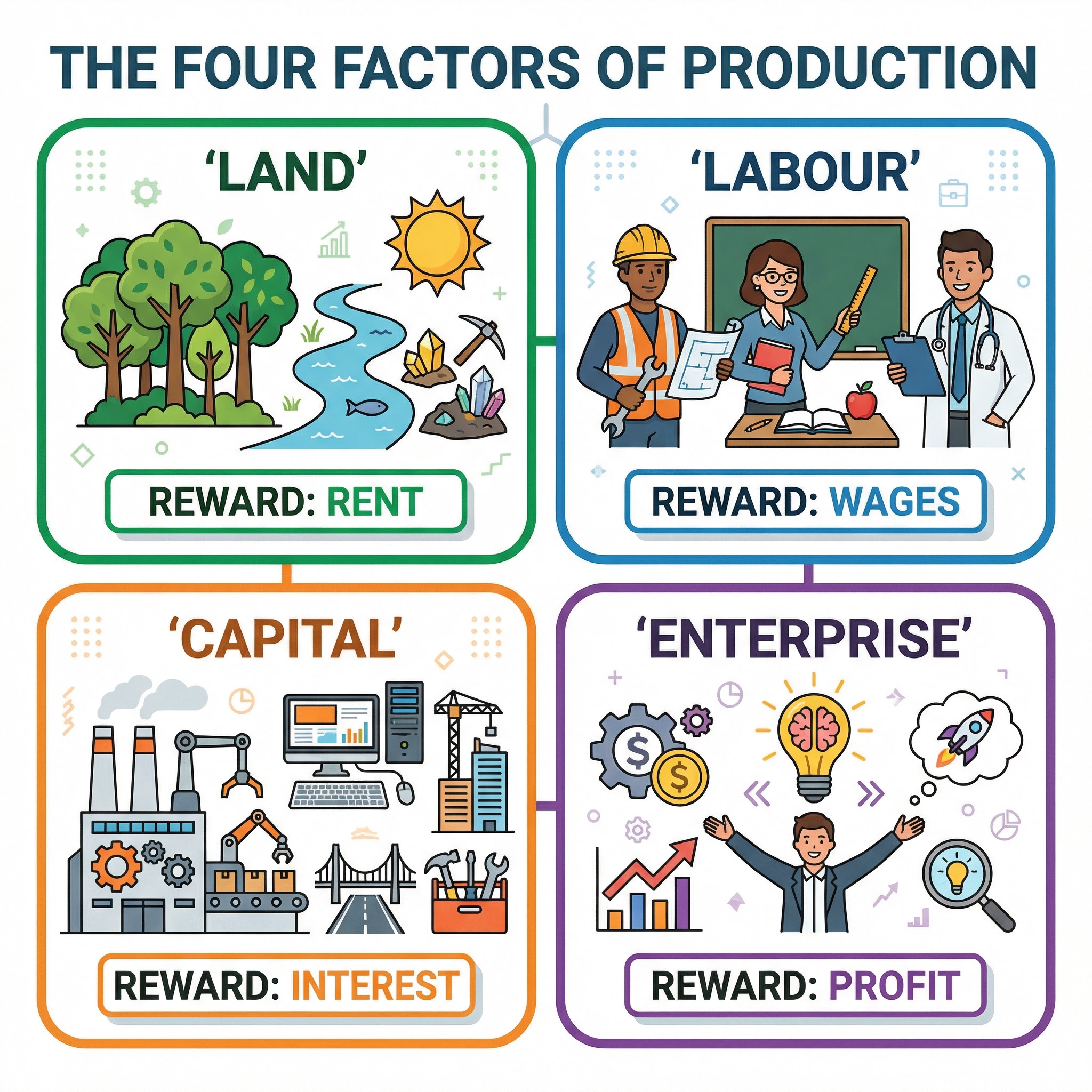

### The Four Factors

These are the economic resources used to produce goods and services. A useful mnemonic is **CELL**: Capital, Enterprise, Land, and Labour.

**1. Land**: This refers to all **natural resources** used in production. This includes not just physical land, but also minerals, forests, the sea, and even the air. The reward for owning and using land is **Rent**.

**2. Labour**: This is the **human input** into the production process. It includes the physical and mental efforts of workers, from a construction worker to a brain surgeon. The reward for labour is **Wages** or a salary.

**3. Capital**: This is a key area where candidates often make mistakes. Capital refers to **man-made aids to production**. It is NOT money. Examples include machinery, tools, factories, and infrastructure like roads and bridges. The reward for capital is **Interest**.

**4. Enterprise**: This is the factor that brings the other three together. The entrepreneur is an individual who takes the **risk** of starting a business, organises the other factors, and makes key decisions. The reward for successful enterprise is **Profit**.

## Economic Agents and Their Choices

### Consumers

**Role**: Individuals who purchase goods and services to satisfy their wants.

**Scarcity Faced**: Limited income.

**Example of Opportunity Cost**: A student with £20 has to choose between buying a textbook or going to the cinema with friends. If they buy the textbook, the opportunity cost is the enjoyment and social experience of the cinema trip.

### Producers

**Role**: Firms that produce goods and services.

**Scarcity Faced**: Limited resources (e.g., machinery, skilled workers, raw materials).

**Example of Opportunity Cost**: A car manufacturer can produce either a petrol car or an electric car with its available factory space and labour. If it chooses to produce the electric car, the opportunity cost is the profit it could have earned from producing the petrol car.

### Government

**Role**: A body that governs a country, provides public services, and redistributes income.

**Scarcity Faced**: Limited tax revenue and national resources.

**Example of Opportunity Cost**: The government has a budget of £50 billion for infrastructure. It can choose to build a high-speed railway line or upgrade the national motorway network. The opportunity cost of building the railway is the improved journey times and reduced congestion that the motorway upgrade would have provided.